투자정보

그로버스 컨설팅은 그로버스 회원들을 위해 주식, 부동산 등 다양한 투자 분야의 유익한 정보를 무료로 제공합니다. 고객의 성공적인 투자와 지속적인 부의 성장을 기원합니다.

그로버스 투자정보 서비스의 강점

그로버스 컨설팅은 18년 경력의 금융시장 전문가가 직접 투자 분석을 수행하며, 단순한 정보 제공을 넘어 전문적이고 체계적인 분석을 제공합니다. 깊이 있는 분석과 전문적인 인사이트로, 고객의 자산이 안정적으로 성장할 수 있도록 함께합니다.

1. 국내외 주식투자 정보(U.S. Stock Investment Information)

1. 속설의 배경

월가에는 오래된 격언이 있습니다.

“로쉬 하샤나에 팔고, 욤키푸르에 사라(Sell Rosh Hashanah, Buy Yom Kippur).”

- 로쉬 하샤나(Rosh Hashanah): 유대인의 새해, 9~10월경

- 욤키푸르(Yom Kippur): 대속죄일, 로쉬 하샤나 약 10일 뒤

뉴욕 금융시장에서 유대인 투자자 비중이 컸던 시절, 명절 기간의 유동성 공백이 시장 변동성과 연결된 데서 유래했습니다.

2. 역사적 분석

- S&P 500 지수(1971년 이후)

- 평균 –0.5% 하락

- 52년 중 29년 실제 하락

- 장기 백테스트 (1928년 이후)

| 지표 | 결과 |

|---|---|

| 누적 수익률 | +39% |

| 연평균 복리수익률 (CAGR) | 0.34% |

| 평균 수익률 (기간당) | +0.39% |

| 승률 | 약 53% |

👉 시장의 장기 평균 수익률(연 8~10%)과 비교 시 매우 미미한 수준, 실질적 투자 전략으로서 의미는 제한적

- 특징적 패턴

- 경기 불안기(대공황, 스태그플레이션)에는 하락이 두드러짐

- 최근 수십 년은 효과 약화, 절반 가까운 해에서 상승 발생

3. 현대 시장에서의 의미

- 신뢰도 한계: 일관성 부족, 장기 성과 미약

- 글로벌화된 시장: 명절 효과는 점차 희석

- 계절적 요인: 9~10월 자체가 변동성이 큰 시기와 겹침

4. 해석과 시사점

- 단순한 투자법보다는 시장 심리·계절성 이해를 돕는 격언

- 매년 9~10월 단기적 유동성 축소와 변동성 확대 가능성을 경계할 필요 있음

5. 결론

“로쉬 하샤나 매도, 욤키푸르 매수”는

- 과거에는 일부 사실로 작동했지만,

- 오늘날에는 문화적·역사적 참고 자료에 가깝습니다.

따라서 투자자들은 이를 절대적 전략이 아닌, 시장 심리와 계절적 흐름을 이해하는 보조 지표로 활용하는 것이 바람직합니다.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

핵심 요약

- 단기(8–9월): 계절적 약세·유동성 축소·고용지표 변수로 10–15% 조정 가능성 확대

- 중기(Q4 2025): 실업률이 안정되면 연준 완화 전환 → 반등 가능성

- 장기(2026–2027): 관세·보호무역 리스크가 성장 훼손 시 구조적 약세 위험 ↑, 다만 정책 완화 시 회복 여지

- 전략: 9월 전까지 현금비중 상향, 하락 시 우량 성장주 분할 매수 준비

1) 현재 시장 환경

- 나스닥·S&P 500은 사상 최고치 부근, 밸류에이션 부담 지속

- 미국 실업률: 저점 대비 완만한 상승(약 4.1~4.3%) → 추세 전환 가능성 경계

- 10년물 국채금리 4%+: 주식의 멀티플 확장 여지 제한

2) 핵심 위험 지표

- 실업률 추세: 4.5~5%로 지속 상승 시 경기둔화 신호 강화

- 레버리지: 높은 마진잔고 → 하락 시 변동성 증폭

- 신용 스트레스: 소비 연체·하이일드 스프레드 확대 조짐 점검

- 이익 전망: 애널리스트 EPS 리비전 둔화 여부 체크

3) 단기 전망 (2025년 8–9월)

- 계절성: 1928년 이후 9월은 통계적으로 가장 약한 달

- 유동성: 명절 전 현금 수요·기업 지급 이벤트 → 유동성 스퀴즈 가능

- 트리거: 9월 5일(금) 고용보고서가 방향 가를 핵심 이벤트

평가: 단기 조정(약 10–15%) 확률 상승

4) 중기 전망 (Q4 2025)

- 실업률이 현 수준 부근에서 안정되고, 연준이 완화적 스탠스 전환 시

- 리스크자산 반등 가능성:

- 미국 빅테크

- 바이오/헬스케어

- 글로벌 경쟁력 보유 한국 소비·수출주(K-뷰티, 엔터 등)

5) 장기 전망 (2026–2027)

- 무역정책 리스크(관세/보호무역) 장기화 시 이익·멀티플 동시 압박

- 실업률 상승 동반 시 구조적 약세(-30%~ -50%) 위험 커짐

- 다만 금리 인하·정책 조정 진행 시 2026 이후 회복 국면 진입 가능

6) 실행 전략(플레이북)

지금(8–9월 전)

- 현금비중 상향, 레버리지 축소

- 손절·리밸런싱 사전 원칙 명문화(가격·지표 트리거)

하락 발생 시

- 분할 매수: 우량 성장주 중심, 2~4회에 나눠 진입

- 신용스프레드·실업률 추가 악화 없을 때만 규모 확대

관찰해야 할 체크리스트

- 실업률: 4.5% 상회 여부 및 연속 상승

- 하이일드 스프레드: 확대 지속 여부

- EPS 컨센서스: 하향 전환 폭

- 정책: 연준 완화 신호(점도표·가이던스)

7) 결론

- 단기: 방어적 포지션 유지, 이벤트 리스크(9/5 고용) 대비

- 중기: 연준 완화+고용 안정 시 연말 랠리 가능

- 장기: 관세·실업 충격 관리 필요, 정책 정상화 시 회복 시나리오 유효

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

2025년 8월 20일 미국 증시 분석 보고서

요약

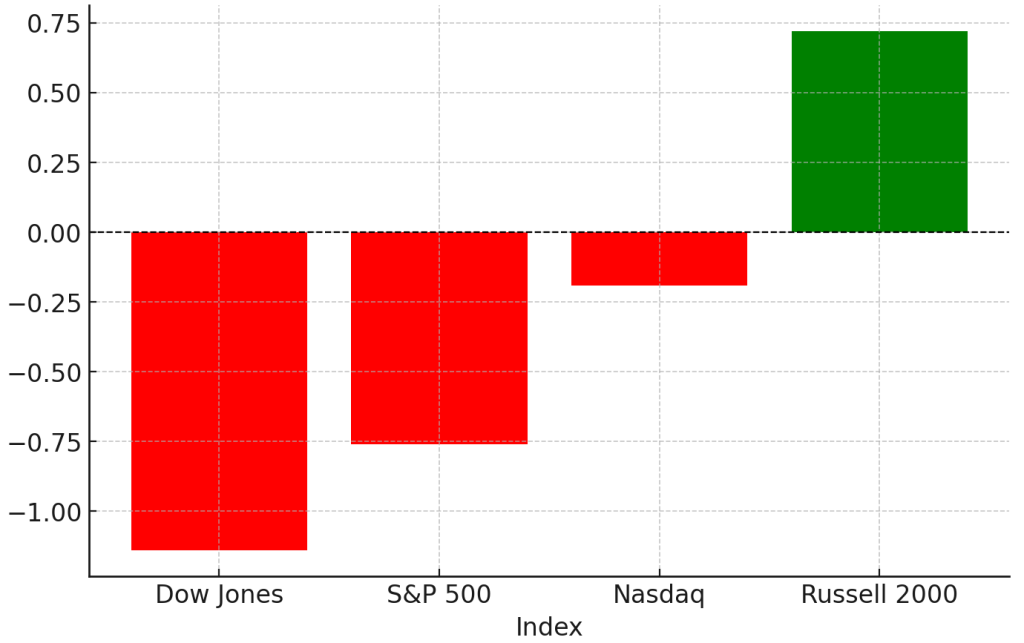

- 지수 마감: S&P 500 -0.2% (6,395.78), 나스닥 -0.7% (21,172.86), 다우 +0.1% 미만 (44,938.31), 러셀 2000 -0.3% (2,269.35). 기술주 약세 속 장중 저점 대비 낙폭 축소 후 마감. AP News

- 스타일 변화: 투자자들이 **고평가 기술주 → 상대적으로 저평가 섹터(에너지·헬스케어·필수소비재)**로 회전. 잭슨홀(8/21–23) 연준 발언 대기. Reuters

- 연속 하락: S&P 500, 4거래일 연속 하락. 기술주 중심 조정 지속. InvestopediaBloomberg.com

지수 & 섹터

- 종가 기준: S&P 500 6,395.78 (-0.2%), 나스닥 21,172.86 (-0.7%), 다우 44,938.31 (+0.1% 미만), 러셀 2000 2,269.35 (-0.3%). AP News

- 섹터 동향: 기술·임의소비재 약세, 에너지·헬스케어·필수소비재 강세. 고평가 기술주 차익실현과 방어주 선호가 맞물림. Reuters

거시 변수

- 연준/잭슨홀: 투자자들은 잭슨홀에서의 연준 스탠스(물가 위험 vs 고용 둔화)를 주시. 최근 커뮤니케이션은 물가 리스크를 더 중시하는 뉘앙스로 해석돼 기술주 밸류에이션 압박. Bloomberg.com

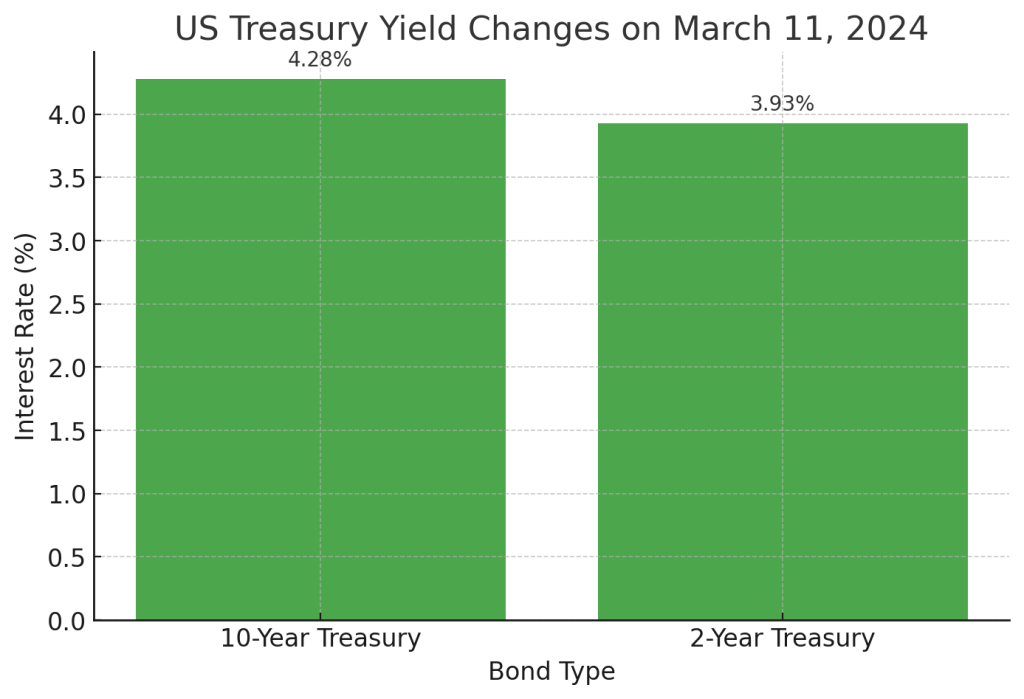

- 채권·달러: 미 10년물 금리 약 3.29% 근처로 보합, 2년물은 소폭 하락. Reuters

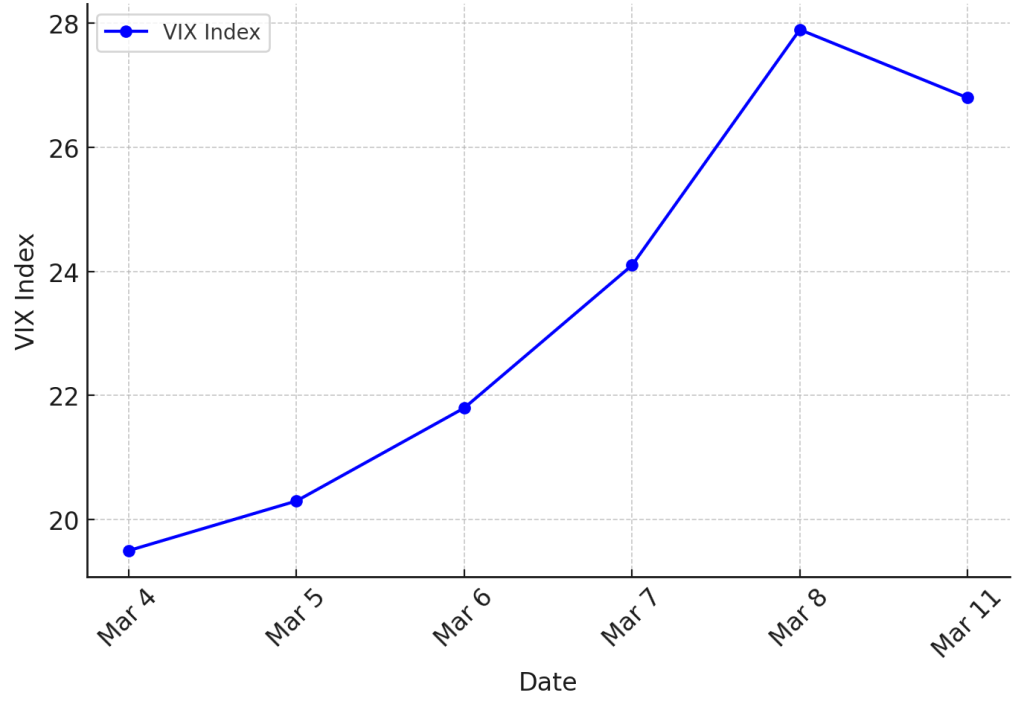

- 변동성: VIX 선물 **15.57(8/20 결제)**로 중저위 변동성 구간 유지. cboe.com

- 원유: 재고 감소 영향으로 Brent +1.6%→ $66.84, WTI +1.4%→ $63.21로 상승 마감. Reuters

종목 포인트

- 타깃(Target): 실적 부진·내부 승계형 CEO 발표 여파로 급락, 투자자 실망감 반영. The Wall Street Journal

- 에스티 로더(EL): 연간 이익 가이던스 하회, 관세로 2026년 약 1억 달러 타격 경고 → 주가 약세. Reuters

- TJX: 분기 실적/가이던스 상향으로 사상 최고가 경신. 오프프라이스 소매 강세 확인. Reuters

- Analog Devices(ADI): 실적 서프라이즈 및 가이던스 상향 → 주가 강세. analog.com

- (참고) 팔란티어: 장중 급락 후 낙폭 축소, 기술주 전반 조정 속 종목별 변동성 확대 지속. Investors

해석

- 밸류에이션 압력: 기술주 중심의 고평가 구간에서 연준의 “물가 경계” 메시지와 잭슨홀 이벤트 리스크가 단기 조정 요인으로 작동. ReutersBloomberg.com

- 방어적 회전: 에너지·헬스케어·필수소비재로의 회전은 리스크 축소 의지 반영. 단, 금리·원유 추세 변화에 민감. Reuters+1

- 변동성/유동성: VIX 중저위, 10년물 보합은 패닉 신호 부재를 시사하나, 빅테크 조정의 연쇄 효과는 단기 이어질 소지. cboe.comReuters

체크리스트 (향후 1주)

- 잭슨홀(8/21–23) 파월 의장 발언: 완화 시사 vs 물가 우려 균형. Reuters

- 대형 기술주 뉴스플로우: 가이던스·규제·관세/정책 변수 점검. Bloomberg.com

- 원유/금리: 유가 상승 지속 시 인플레 재가열 우려, 금리 재상승 리스크. Reuters

전략(요약)

- 단기: 기술주 비중 축소·방어주/현금 비중 상향, 이벤트(잭슨홀) 이전 리스크 관리.

- 선별 매수: 실적 모멘텀 확인된 방어·퀄리티 팩터(예: TJX, 일부 의료·필수소비재), 실적 서프라이즈 반영된 반도체 내 비메가캡 (사례: ADI) 위주로 분할 접근. Reutersanalog.com

- 모니터링: 10년물 금리·유가·VIX가 동시에 상방일 경우 리스크 감축 강화

2025년 8월 20일(수) 한국 증시 분석

증시 마감 요약

- 코스피: 3130.09p로 마감, 전일 대비 –0.68% 하락. (turn0search19)

- 코스닥: 777.61p, –1.31% 하락. (turn0search19)

- 3거래일 연속 하락세, 지수 하락폭 약 3% 누적. (turn0search17)

원인 분석

- 기술주 중심 급락 여파

미국 기술주 중심의 조정이 아시아 전반, 특히 한국 증시에도 직격되어 코스피가 1.7% 하락. (turn0news29, turn0news30) - 외국인 매도세 유입

지수 하락 흐름 속에서 외국인과 개인 모두 매도 전환하며 순매도 강화. (turn0search19) - 잭슨홀 회의 대기 심리

연준의 향후 금리 기조 방향에 대한 불확실성이 커지며, 기술주 중심의 리스크 관리 흐름으로 전환. (turn0search7) - 반도체 수출주 약세 및 지정학 리스크

반도체 관련 주가 약세에 따른 전반적 하방 압력, 여기에 한반도 지정학 불안도 투자 심리 위축 요소로 작용. (turn0search7)

향후 주요 모멘텀

- 글로벌 정책 이벤트인 잭슨홀(8/21~23) 연설이 투자 심리의 향배를 결정할 변수.

- 반도체 업종과 수출주 실적·공급망 동향, 지정학 리스크 등도 주가 향방에 영향.

요약 & 전략 제언

| 구분 | 요약 내용 | 전략 제안 |

|---|---|---|

| 단기적 대응 | 기술주 중심 하락과 외국인 매도세 확대, 상승 모멘텀 약화 | 현금 비중 확보 및 방어주 중심 분할 매수 추천 |

| 리스크 포인트 | 지정학 불안, 글로벌 정책 불확실성 | 포지션 청산 기준 설정 및 유동성 확보 필요 |

| 기회 포착 | 하락 시 글로벌 밸류주 또는 수출주 중심 리밸런싱 가능성 | 저점 매수 타이밍 신중 예측 및 대응 |

요약하면, 8월 20일은 기술주 중심의 해외 영향과 외국인 매도 압력으로 국내 지수가 하락한 날이며, 잭슨홀 회의 발표 전 불확실성 관리 차원에서 차분한 대응이 필요합니다.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

미국 증시 요약 (2025년 8월 19일)

- S&P 500

- 종가: 6,411.37p, –0.6% 하락

- 3거래일 연속 하락, 최근 사상 최고점 대비 조정 국면 Nasdaq+7Reuters+7Bloomberg.com+7AP News+2Midland Daily News+2MarketWatch+1

- 나스닥 종합지수

- 종가: 21,314.95p, –1.5% 하락

- AI 관련 기술주들(팔란티어, 엔비디아 등) 중심의 급락이 주요 원인 AP News+1

- 다우존스 산업평균지수

- 종가: 44,922.27p, +0.1% 상승

- 홈디포 실적의 안정적인 가이던스로 지지 Korea Herald+15AP News+15MarketWatch+15Korea Herald

- 러셀 2000

- 종가: 2,276.61p, –0.8% 하락 Reuters+15AP News+15The Wall Street Journal+15

- 주요 테마 및 섹터 흐름

- 기술주 약세, 투자자들은 **방어 섹터(부동산, 유틸리티, 필수소비재)**로 회전 중 The Wall Street Journal

- 주택 착공 증가: 경기 전환 기대감 조성. 실적 부진에도 홈디포는 강세. The Wall Street JournalInvestors

- 기타 종목 이슈: 팔란티어 –9.4%, 엔비디아 –3.5%, 페이스트널 등 일부 기업 낙폭 확대. 반면 인텔 +6%, 팔로알토네트웍스 +5~6% 등은 상승 Investors

- 유동성 조건: 낮은 거래량이 단기 변동성 확대에 기여 The Wall Street Journal

한국 증시 요약 (2025년 8월 19일)

- 코스피 지수: 3,185p 부근에서 이틀 연속 하락, 약 –2.4% 하락세 누적 Nasdaq+15Nasdaq+15RTTNews+15

- 배경 요인: 미국 기술주 조정 영향으로 한국 기술주 중심의 매도세 확대

- 관련 타격: 외국인 투자자 수급 약화 및 글로벌 불확실성 대응 차원에서 보수 전략 강화 중으로 보임

요약 정리

| 시장 | 주요 포인트 |

|---|---|

| 미국 | 기술 섹터 중심의 급락 → 방어 섹터로 자금 이동 / 연속 하락세, 단기 불확실성 증대 |

| 한국 | 코스피 약세 전환, 미국 IT 충격 확산 / 외국인 투자 흐름 변화가 시장 방향성에 큰 영향 |

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

< 미국 증시 >

1. 시장 개요 (Market Overview)

8월 18일 미국 주식시장은 전반적으로 혼조세를 보이며 큰 변동 없이 마감했습니다.

- 다우존스 산업평균지수는 소폭 하락했고,

- S&P 500은 거의 보합세,

- 나스닥은 소폭 상승세를 기록했습니다.

여름철 비수기 특성과 더불어 이번 주 발표 예정인 연준 의사록(FOMC Minutes), 잭슨홀 미팅 파월 의장 연설 등을 앞둔 관망세가 짙게 나타났습니다.

2. 주요 지수 동향 (Major Index Performance)

| 지수명 | 종가 변동 | 변동률 | 특징 |

|---|---|---|---|

| 다우존스 (DJIA) | 약 –33pt | –0.08% | 보잉, Sherwin-Williams 부진 |

| S&P 500 | –0.65pt | –0.01% | 거의 변화 없음 |

| 나스닥 (Nasdaq) | +6.8pt | +0.03% | 일부 빅테크 및 헬스케어 종목 지지 |

| 러셀 2000 (소형주) | +0.3% | 상승 | 소형주 강세 지속 |

3. 업종 및 종목별 동향 (Sector & Stock Highlights)

▲ 강세 종목/업종

- 클린에너지주:

- First Solar (+9.7%), Sunrun (+11%)

→ 세제 혜택 기대감으로 급등

- First Solar (+9.7%), Sunrun (+11%)

- 헬스케어:

- UnitedHealth Group: 버크셔 해서웨이 투자 소식에 상승

- Novo Nordisk: 비만 치료제 Wegovy 간 질환 적응증 FDA 승인 → +3.7% 급등

- 호텔/레저:

- Soho House: MCR 주도 인수 발표 → +14.9% 급등

▼ 약세 종목/업종

- 빅테크 일부: Meta –2.3% (스마트글라스 가격 인하 우려)

- 항공/제조: Boeing –1% 이상 하락

- 건축·소재: Sherwin-Williams –1%대 하락

4. 거시경제 및 정책 요인 (Macroeconomic & Policy Factors)

- 연준(Fed) 정책 기대

- 투자자들은 이번 주 공개될 FOMC 의사록과 잭슨홀 파월 의장 연설에서 금리 인하 신호를 기대하며 관망세 유지.

- 채권시장

- 미 10년물 국채금리: 4.33% 수준에서 안정적 흐름.

- 거래량

- 여름 비수기 속에서 5월 이후 최저 거래량 기록.

5. ETF 동향 (ETF Performance Snapshot)

| ETF | 가격(USD) | 변동 | 특징 |

|---|---|---|---|

| SPY (S&P 500) | 643.3 | –0.07 | 지수와 동일하게 보합세 |

| QQQ (Nasdaq 100) | 577.1 | –0.21 | 소폭 약세 |

| DIA (Dow ETF) | 449.05 | –0.39 | 다우 약세 반영 |

6. 향후 전망 (Outlook)

- 단기적: 관망세 지속, 변동성 낮을 전망

- 중기적:

- 클린에너지·헬스케어 섹터 강세 가능성

- 연준의 통화정책 방향(금리 인하 가능성)에 따라 9월 이후 방향성 확대 예상

7. 결론 (Conclusion)

8월 18일 미국 증시는 큰 방향성 없이 보합세를 유지했으며,

업종별로는 클린에너지와 헬스케어가 뚜렷한 강세, 반면 항공·소재·일부 빅테크는 약세를 기록했습니다.

투자자들은 이번 주 예정된 연준 의사록과 잭슨홀 미팅에 초점을 맞추고 있으며,

향후 정책 시그널에 따라 시장의 변동성이 확대될 가능성이 큽니다.

< 국내 증시 >

1. 시장 개요

- KOSPI 지수 마감: 전 거래일 대비 –48.38포인트, –1.5% 하락한 3,177.28포인트로 마감하며, 이틀간 이어졌던 상승 흐름 종료 koreajoongangdaily.joins.comnasdaq.com

- 거래량: 약 3억 1,972만 주, 8.77조원 규모의 매매체결 → 다소 부진한 거래 흐름 koreajoongangdaily.joins.com

- 외국인·기관 투자세: 감소한 반면, 하락 종목이 697개, 상승 종목은 198개로 하락 종목이 크게 우세 koreajoongangdaily.joins.com

2. 주요 원인 및 시장 심리

- 미국의 반도체 수입 관세 우려: 주요 반도체 관련 기업들—특히 삼성전자, SK하이닉스—의 주가 하락이 지수 약세에 영향을 미침 koreajoongangdaily.joins.comaccesswdun.com

- 환율 요인: 원화 약세도 복합적으로 불안 요인으로 작용 koreajoongangdaily.joins.com

- 글로벌 불확실성 지속: 잭슨홀 경제정책 심포지엄을 앞두고 투자 심리가 위축된 상태 koreajoongangdaily.joins.com

3. 주요 종목 움직임 & 시장 구조

| 종목/섹터 | 동향 |

|---|---|

| 삼성전자 | 소폭 반등 (+0.29%) |

| SK하이닉스 | 소폭 상승 (+0.28%) |

| LG에너지솔루션 | 보합 수준 (+0.13%) |

| 동반 상승했으나, 시장 전체에 긍정적 영향을 크게 끼치지는 못함 koreajoongangdaily.joins.com |

4. 시장 평가 및 밸류에이션

- 한국 전체 시장 PER(주가수익비율): 약 14.2배, 3년 평균(17.3배)보다 낮아 상대적으로 저평가된 모습 simplywall.st

- 시장 캡 규모: 총 시가총액 약 ₩2,968.9조 / 매출 약 ₩3,764.1조 / 이익 ₩178.1조 기준 simplywall.st

5. 대외 환경 및 정책 요소

- 미국의 반도체 관세 이슈– 한국 증시에 부정적 영향 발생 koreajoongangdaily.joins.comaccesswdun.com

- 정치·사회적 불확실성– 최근 선거 이후 정책 및 규제 변화에 대한 불확실 성 존재 en.wikipedia.org+1

- 제도적 시장 개선 노력– 접속 시간 연장 등 거래제도 개선 시도 중 (블로그 요약) rising-k-stocks.tistory.com

6. 간략 요약 (Executive Summary)

- 하락 원인: 반도체 업종 중심의 불확실성, 외국인 투자 심리 위축, 글로벌 불확실성 확대

- 시장 평가: PER 기준 시장은 평균보다 낮아 여전히 저평가 여지 존재

- 정책 기대: 반도체 정책 대응, 글로벌 무역 긴장 완화, 거래체계 개편 등 향후 개선 여력 상존

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

< 미국 증시 >

▸ 지수 마감 현황

| 지수 | 종가 | 등락폭 | 등락률 |

|---|---|---|---|

| 다우존스 산업평균지수 (DJIA) | 40,432.67 | ▲139.02 | +0.34% |

| S&P 500 지수 | 5,470.55 | ▼3.16 | -0.06% |

| 나스닥 종합지수 | 17,832.63 | ▼28.25 | -0.16% |

| 러셀 2000 (소형주) | 2,195.48 | ▲22.45 | +1.03% |

※ 종가 및 수치는 대표 금융 미디어 기준으로 요약됨

▸ 시장 특징 및 핵심 이슈

✅ 실적 시즌 호조 지속

- S&P 500 기업들의 실적이 전년 대비 약 12% 증가, 이는 애널리스트들의 평균 전망치(5%)를 두 배 이상 상회.

- AI·반도체 관련 기술주가 실적 상승을 견인하며 시장 전반의 낙관론을 부각.

✅ 다우지수, 경기방어주 및 금융주 중심 강세

- 버크셔 해서웨이 등 금융·산업주 중심의 강세 흐름.

- 전통 가치주 중심의 순환매 흐름이 반영됨.

✅ 기술주 혼조세

- 나스닥 지수는 차익실현 매물로 약세. 메타, 엔비디아, 테슬라 등 일부 종목이 조정받음.

- 반면 일부 AI 관련 종목은 견조한 실적에 힘입어 강보합세 유지.

✅ 시장 집중화 우려

- S&P 500 시가총액 상위 10개 종목이 전체 비중의 약 40% 차지.

→ 지나친 대형 기술주 쏠림에 따른 리스크 경고도 시장 내부에서 제기.

▸ ETF·섹터 흐름

- ARK Innovation ETF: +8% 급등 (유전체학 및 AI 테마 강세)

- XLF (금융 섹터 ETF): +0.9%

- XLK (기술 섹터 ETF): -0.3%

▸ 투자자 정서 및 전망

- 시장은 다음 주 예정된 잭슨홀 심포지엄에서의 파월 의장 연설에 주목하며 관망세 확대.

- 금요일 마감은 전반적으로 실적 호조에 따른 펀더멘털 기반의 상승세가 주를 이룸.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

< 미국 증시 >

주요 지수 요약

- S&P 500 지수는 소폭 상승하며 사상 최고치 종가를 경신했습니다.Yahoo Finance+5AP News+5The Wall Street Journal+5

- **다우존스 산업평균(Dow Jones)**와 **나스닥(Nasdaq)**은 거의 변동 없이 보합권 마감했습니다.Wikipedia+1

- 러셀 2000 소형주 지수는 1.2% 하락했습니다.AP News

시장 동향 및 주요 요인

1. 예상보다 높은 생산자물가 지표 (PPI) 충격

- **7월 생산자물가지수(PPI)**는 0.9% 급등, 3년 만에 가장 큰 상승 폭으로 핫한 인플레이션 우려를 불러왔습니다.Barron’s+4Reuters+4Schwab Brokerage+4

- 이로 인해 연준의 9월 금리 인하 가능성 기대감이 약화되었고, 시장 전반 분위기에도 제동이 걸렸습니다.Yahoo Finance+6AP News+6The Wall Street Journal+6

- 이에 따라 장기 국채 수익률 상승과 함께 투자자들의 리스크 인식이 강화되었습니다.The Wall Street JournalReuters

2. 빅테크 중심의 하방 방어

- 전반적으로 증시가 흔들리는 가운데, 아마존(Amazon) 등 일부 핵심 기술주가 상승하며 시장을 안정시키는 역할을 했습니다.AP NewsThe Washington PostSpectrum Local News

3. 개별 종목 소식

- CoreWeave (CRWV): –15.5% 급락, 하루 거래량 52억 달러 규모로 12위 규모의 대규모 매도 발생.AInvest

- Tapestry (Coach 브랜드): 관세로 인한 비용 증가 우려에 –15.7% 하락.AP News

요약 : 8월 14일 미국 증시 주요 요인

| 항목 | 내용 |

|---|---|

| S&P 500 | 소폭 상승, 종가 기준 사상 최고치 |

| Dow Jones / Nasdaq | 보합권 마감 (변동 거의 없음) |

| Russell 2000 | –1.2% 하락 |

| PPI (생산자 물가) | +0.9% 급등, 인플레이션 우려 촉발 |

| 금리 인하 기대 | 후퇴 (연준의 금리 인하 전망 약화) |

| 시장 분위기 | 불확실성 증대, 리스크 회피 심리 강화 |

| 빅테크 | 시장 방어 중심 역할 (아마존 등 상승 주도) |

| 개별 주식 | CoreWeave –15.5%, Tapestry –15.7% |

해석 및 인사이트

- 인플레이션 리스크 재부각: PPI의 급등은 연준의 정책 스탠스를 흔들며 단기 부정적 영향을 미쳤습니다.

- 시장 반응은 제한적: S&P는 기록적 종가를 재차 경신하며 저항력을 보여줬고, Dow와 Nasdaq은 보합권에서 진정 상황을 나타냈습니다.

- 금융 시장 불확실성 확대: 금리 인하 기대가 조정되며 투자자들은 더 신중한 수급 전략을 요구받고 있습니다.

- 테크 기업의 구조적 중요성: 빅테크 주도 장세는 기술주 중심의 집중도가 여전히 높음을 의미합니다.

- 리스크 관리 중요: CoreWeave와 Tapestry 사례처럼 개별 기업 리스크에 따른 급등락 발생 가능성 있음.

< 한국 증시 >

주요 지수 및 환율 – 8월 14일 마감

- 코스피(KOSPI): 전일 대비 +1.29포인트(+0.04%) 상승한 3,225.66포인트로 마감 contents.premium.naver.com+10newsis.com+10wealthstockbriefing.com+10.

- 코스닥(KOSDAQ): 전일 대비 +1.16포인트(+0.14%) 상승한 815.26포인트로 마감 newsis.com+1.

- 원·달러 환율: 전일(1,381.7원)보다 0.3원 상승한 1,382.0원에 마감 조선일보+10newsis.com+10wealthstockbriefing.com+10.

수급 동향

- 코스피 시장:

- 기관: 약 169억 원 순매수하며 지수를 지탱.

- 개인 및 외국인: 각각 530억 원, 781억 원 순매도 Investing.com 한국어+3g-enews.com+3wealthstockbriefing.com+3.

- 코스닥 시장:

- 외국인 및 기관: 각각 514억 원, 18억 원 순매수.

- 개인 투자자: 322억 원 순매도 wealthstockbriefing.com+3g-enews.com+3Investing.com 한국어+3Investing.com 한국어.

업종 및 주요 종목 흐름

코스피 주요 업종

- 강세 업종:

- 통신 (+1.5%), 보험 (+1.2%), 일반서비스 (+1.0%), 화학 (+0.6%) wealthstockbriefing.com+1.

- 약세 업종:

- 전기·가스, 의료정밀기기, 부동산, 음식료·담배 등에서 하락세 관측 newsis.com+1.

시가총액 상위 종목 흐름

- 상승 종목:

- LG에너지솔루션 (+1.16%), 한화에어로스페이스 (+0.57%), 현대차 (+0.69%), HD현대중공업 (+2.14%) Investing.com 한국어+3newsis.com+3wealthstockbriefing.com+3.

- 하락 종목:

- 삼성전자 (–0.42%), SK하이닉스 (–0.54%), 삼성바이오로직스 (–0.67%), 삼성전자우 (–1.19%), KB금융 (–1.22%), 두산에너빌리티 (–1.50%) Investing.com 한국어+3newsis.com+3wealthstockbriefing.com+3.

코스닥 주요 종목 흐름

- 상승 종목:

- 에이비엘바이오 (+7.11%), 파마리서치 (+2.86%), 에코프로 (+2.45%), 에코프로비엠 (+1.68%), 펩트론 (+1.29%), 레인보우로보틱스 (+0.93%), 리가켐바이오 (+0.32%) newsis.com+3g-enews.com+3Investing.com 한국어+3.

- 하락 종목:

- 알테오젠 (–2.67%), HLB (–1.08%), 삼천당제약 (–0.48%) newsis.com+3g-enews.com+3Investing.com 한국어+3.

시장 현황 요약

| 항목 | 내용 |

|---|---|

| 지수 흐름 | 코스피 +0.04%, 코스닥 +0.14% |

| 수급 특징 | 코스피: 기관이 매수 지지 / 코스닥: 외국인·기관 매수, 개인 매도 |

| 업종 흐름 | 통신·보험·서비스·화학 강세, 기타 업종 약세 |

| 주요 종목 흐름 | LG·현대차 등 상승, 삼성·SK 등 하락 |

| 코스닥 테마주 | 제약·바이오·이차전지 개선 |

| 환율 흐름 | 소폭 상승(1,382원) |

| 시장 환경 | 상승 모멘텀 부재, 기관 수급 중심 장세 |

해석 및 인사이트

- 약보합 속 관련 수급 주도 전개

코스피는 전반적으로 뚜렷한 모멘텀 없이 횡보했고, 기관의 순매수가 지수 하방을 방어한 장세로 보입니다 조선일보+6Investing.com 한국어+6wealthstockbriefing.com+6wealthstockbriefing.com+1경향신문+5g-enews.com+5wealthstockbriefing.com+5. - 코스닥은 테마주 중심 상승

바이오·이차전지 등의 종목이 강세를 보이며 지수를 견인했지만, 전반적으로는 개인 매도 우위, 외국인·기관 매수 흐름이 이어졌습니다 wealthstockbriefing.com. - 증시 활동성 저하 지속

8월 국내 증시는 박스권 흐름이 이어지면서 시가총액 회전율이 연중 최저 수준으로 하락했습니다.- 유가증권시장 회전율: 4.14%

- 코스닥 회전율: 12.16%

- 합산 일평균 거래대금 약 15조~16조 원으로 6월 대비 상당히 낮은 수준 contents.premium.naver.com+6hani.co.kr+6v.daum.net+6.

- 중장기적 대응 권고

시장이 저변동성, 제한된 유동성 환경에 놓여 있으므로 단기 대응보다 중장기 시각의 관망 전략, 테마 기반 분산투자가 유효하다는 평가가 나옵니다 hani.co.kr경향신문.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

< 미국 증시 >

주요 지수 종가 (8월 13일 기준)

- S&P 500 (스탠다드앤드푸어스 500 지수)

종가: 6,466.58, 전일 대비 +0.3% / +20.82포인트 증가—사상 최고치 경신 Reuters+8Yahoo Finance+8Reuters+8Reuters+1AP News+1. - Dow Jones 산업평균지수 (다우)

종가: 44,922.27, 전일 대비 +1.0% / +463.66포인트 상승 AP News. - Nasdaq 종합지수

종가: 21,713.14, 전일 대비 +0.1% / +31.24포인트, 이 역시 사상 최고치 경신 Reuters+11AP News+11Wikipedia+11. - 러셀 2000 소형주 지수

종가: 2,228.06, 전일 대비 +2.0% / +45.28포인트 상승 AP News+1.

요약 테이블

| 지수 | 종가 | 변화 | 최고치 여부 |

|---|---|---|---|

| S&P 500 | 6,466.58 | +0.3% (+20.82) | 사상 최고치 달성 |

| Dow Jones | 44,922.27 | +1.0% (+463.66) | — |

| Nasdaq | 21,713.14 | +0.1% (+31.24) | 사상 최고치 달성 |

| Russell 2000 | 2,228.06 | +2.0% (+45.28) | — |

시장 주요 흐름 요약

- 금리 인하 기대 강화: 연준의 9월 금리 인하 가능성에 대한 시장 기대감이 커지며 S&P 500과 Nasdaq이 이틀 연속 최고치 경신 morningstar.com+15Reuters+15Wikipedia+15Wikipedia+5AP News+5Wikipedia+5.

- 투자자 심리 개선: 인플레이션 둔화 신호, 낮은 변동성(VIX 약 14.4), 그리고 글로벌 주요 증시 동반 상승 등이 투자 심리를 뒷받침 thetimes.co.uk.

- 섹터별 특징:

- 헬스케어: +1.6% 강세 Reuters.

- 항공주: United Airlines (UAL) +1.34%, 같은 날 Delta +1.68%, Southwest +0.81%, American +1.00% MarketWatch.

- 미디어 및 엔터테인먼트: Paramount Skydance +37% (UFC 방송권 확보), Warner Bros. Discovery +7.4% (동남아 스트리밍 번들) Investopedia+1.

- 건설: PulteGroup +5.4%, Lennar +5.2% (금리 인하 기대에 따른 모기지 비용 완화 전망) Investopedia+2Reuters+2.

- e‑커머스: Amazon +1.4% (식료품 당일 배송 확대 발표), Kroger –4.4%, DoorDash –3.8% Investopedia.

- 기술주 일부 부진: Nvidia, Alphabet, Microsoft 등 흔히 “Magnificent Seven”으로 불리는 종목들은 다소 조정세 Reuters+1.

- 코어위브(CoreWeave): 실망스러운 실적 발표로 –21% 하락 Reuters+2Investopedia+2.

- IPO 시장 – Bullish (암호화폐 거래소) 뉴욕증시 데뷔, 시가총액 약 131억 달러, 주가 2배 이상 급등

< 한국 증시 >

KOSPI (코스피) 종합지수 – 8월 13일 마감

- 종가: 3,224.37 포인트, 전일 대비 +34.46포인트(+1.08%) 상승 Times UnionBloomberg.com+3koreajoongangdaily.joins.com+3Investing.com+3

- 거래량: 3억 1,640만 주, 거래대금 약 10.2조 원 (약 7.39억 USD) koreajoongangdaily.joins.com

- 장 초반 흐름: 장 시작 15분 내 0.81% 상승, 3,215.59 포인트로 출발 finance.yahoo.com+8koreajoongangdaily.joins.com+8Investing.com+8

시장 배경 및 요인

- 3거래일 연속 하락세 후 반등: 연속된 하락세(bearish)가 이어지다, 당일 환율·외국인 투자자 매수 기대감에 힘입어 강한 반등세 koreajoongangdaily.joins.comRTTNews

- 미국 금리 인하 기대: 미국의 소비자물가지수(CPI)가 시장 기대보다 양호하게 발표되며, 연준의 금리 인하 기대가 강화되어 외국인 매수세 유입 whec.com

- 아시아 증시 상승 흐름 동조: 일본 니케이, 홍콩·싱가포르 등 주요 아시아 증시도 함께 상승하며 긍정적 지역 분위기 조성 WJXTwhec.com

종합 요약

| 항목 | 수치 및 설명 |

|---|---|

| 종가 | 3,224.37 (+1.08%, +34.46포인트) |

| 거래량 | 약 3억 1,640만 주 |

| 거래대금 | 약 10.2조 원 (약 7.39억 USD) |

| 초반 흐름 | 장 초반 0.81% 강세 (3,215.59 포인트) |

| 배경 요인 | 금리 인하 기대·외국인 매수세 유입 |

| 전반적 분위기 | 아시아 증시 동반 상승, 시장 심리 개선 |

인사이트 및 시사점

- 단기 반등의 징후: 3거래일 하락세 이후 금리 인하 기대와 외국인 수급으로 코스피가 강한 반등세를 보이며, 단기 기술적 바닥 가능성.

- 외국인 자금 동향 주목: 외국인 매수세 유입이 반등의 핵심 동인으로, 향후 추가적인 수급 흐름이 관전 포인트.

- 미 연준 정책의 영향력 지속: 미국의 금리 움직임이 국내 증시 방향을 주도하는 구조가 강화된 양상.

- 거래대금 및 유동성 중요: 비교적 건강한 거래대금 수준(10.2조 원)은 시장 회복 탄력성에 긍정적.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

🧭 요약 Summary

2025년 5월 첫째 주는 두 가지 강력한 시장 변수로 인해 단기 변동성 확대가 예상됩니다.

- 트럼프 전 대통령의 외국 영화에 대한 100% 관세 부과 발언과

- 이번 주 중 예정된 연방준비제도(Fed) 회의 및 파월 의장 발언입니다.

시장 참가자들은 정치적 심리전과 통화정책 가이던스 사이에서 방향을 탐색하는 흐름을 보일 것으로 전망됩니다.

🔥 핵심 이슈 분석

1. 🇺🇸 트럼프 “외국 영화 100% 관세” 발언 – 정치인가, 압박 전략인가?

- 트럼프는 최근 외국 영화에 100% 관세를 부과하겠다는 발언으로 시장을 다시 흔들었습니다.

- 이는 자신의 정치적 존재감 부각 및 지지층 결집용 발언으로 해석됨과 동시에,

- 연준에 대한 간접적 압박이기도 한 것으로 풀이됩니다:

→ “내가 시장을 흔들 수 있다, 그러니 금리 인하로 경기방어를 해라.” - 투자자들은 실제 관세 실행 가능성보다, 의도된 발언 효과에 더 민감하게 반응하고 있습니다.

2. 🏦 연준 FOMC 회의 대기 – 동결은 기정사실, 발언에 주목

- 이번 FOMC에서는 금리 동결이 유력하지만, 시장은 파월 의장의 발언 수위에 주목하고 있습니다.

- 트럼프의 발언과 최근의 글로벌 수요 둔화, 유가 하락 등은 연준에 대한 금리 인하 압박을 키우고 있습니다.

- 시장은 연말까지 3차례 인하를 반영하고 있으나, 파월이 이를 명확히 지지하지 않으면 실망 매물 가능성 존재합니다.

📊 시장 전망 및 전략 제안

📉 단기 전망: 시장 흔들림 경계

- 트럼프의 발언 → 단기 심리적 충격

- 연준 회의 → 변동성 촉진 요인

- 기술적 과열 구간 → 9일 연속 상승 후 조정 국면

🛡️ 전략적 대응:

📍 1. 현금 및 유동성 확보

- 변동성 확대가 예상되므로, 단기 기회 포착 및 리스크 관리 차원에서 현금 비중을 10~15% 수준으로 상향하는 것이 바람직할 것으로 보입니다.

📍 2. 경기 민감주 중 선별적 접근

- 단기적으로 낙폭 과대 가능성이 있는 IT 대형주(AAPL, MSFT)나 산업재(디어, 캐터필러)에 대한 저점 분할매수 접근 고려할 필요가 있습니다.

- 단, 밸류에이션 부담 높은 성장주는 제외

📍 3. 금리 기대 반영 섹터: 고배당/채권 대체

- 시장이 연준의 인하 가능성을 선반영하고 있으므로, 리츠, 유틸리티, 고배당 주식은 기술적 반등 여지가 있습니다.

- 단, 파월 발언에 따라 단기 급락 가능성도 상존하므로 비중 조절 필수

📍 4. AI/방산/정치 수혜주 주목

- 트럼프 리스크가 장기화되면 방위산업(예: 팔란티어, 록히드마틴)이나 정책 테마주(예: 미디어, 국산화 테마)에 자금이 유입될 수 있습니다.

- AI 기업은 실적 기대치 상향조정 구간이므로 실적 발표 직전까지는 주시할 만합니다.

📌 결론적으로, 기계적으로 방어주에 몰리기보다는

“현금 확보 + 정책 수혜주 + 낙폭과대 대형주 분할매수”

전략이 더 타당하며, 방어주는 금리 불확실성이 해소된 뒤 보완재 성격으로 접근하는 것이 더 논리적입니다.

🧠 Groverse Insight

“트럼프의 관세 카드는 ‘민심이반 시점에 등장했다가 반등 후 재등장하는’ 전형적 패턴입니다. 이는 시장 심리를 뒤흔드는 데는 성공하지만, 결국엔 연준의 태도와 기업 실적이 방향을 결정지을 것입니다..”

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<한글 보고서(Korean Version)>

📈 주요 지수 마감 현황 (2025년 5월 2일 금요일)

| 지수 | 종가 | 변동폭 | 변동률 |

|---|---|---|---|

| S&P 500 | 5,686.67 | ▲82.53p | +1.47% |

| 다우존스 산업평균 | 41,317.43 | ▲564.47p | +1.39% |

| 나스닥 종합지수 | 17,977.73 | ▲266.99p | +1.51% |

미국 증시는 9거래일 연속 상승하며 2004년 이후 최장 상승 랠리를 기록했습니다. S&P 500 지수는 4월 관세 충격 이전 수준을 완전히 회복했고, 기술주 중심의 상승세가 시장을 주도했습니다.

출처: AP통신

💼 주요 기업 실적 요약

🍎 Apple – 2025년 2분기

- 총매출: 954억 달러 (전년 대비 +5%)

- 주당순이익 (EPS): $1.65 (전년 대비 +8%)

- 부문별 매출:

- 아이폰: 468억 달러 (+2%)

- 맥: 79억 달러 (+7%)

- 아이패드: 64억 달러 (+15%)

- 서비스: 267억 달러 (+12%)

- 웨어러블 및 액세서리: 75억 달러 (-5%)

- 기타 사항:

- 1,000억 달러 규모 자사주 매입 발표

- 배당금 4% 인상 (분기당 $0.26)

- 팀 쿡 CEO: “6월 분기에 약 9억 달러의 관세 비용 예상”

- iPhone은 인도에서, 기타 제품은 베트남 생산 전환 중

- 시간 외 주가: -4% 하락

출처: 애플 보도자료, Business Insider

📦 Amazon – 2025년 1분기

- 총매출: 1,557억 달러 (전년 대비 +9%)

- 순이익: 171억 달러 (주당 $1.59, 전년 $0.98 대비 상승)

- 부문별 매출:

- 온라인 스토어: 574억 달러 (+6%)

- AWS(클라우드): 293억 달러 (+17%)

- 광고: 139억 달러 (+19%)

- 전망:

- 2분기 매출 전망: 1,590억~1,640억 달러

- 영업이익 전망: 130억~175억 달러 (예상보다 보수적)

- 관세 관련 리스크:

- 145% 중국산 수입품 관세의 영향으로 제품 가격 상승과 소비자 수요 위축 우려

- 3자 판매자들과 재고 선주문 등으로 대응 중

- 시간 외 주가: 약 2% 하락

출처: Amazon IR

🌐 거시경제 및 정책 동향

미국 고율 관세 정책

- 트럼프 정부의 145% 중국산 관세가 본격 발효되며, 애플·아마존 등 소비재 중심 기업에 부담 증가

- 공급망 다변화(인도·베트남 이전) 및 재고전략 조정이 핵심 대응책으로 작동 중

출처: Bloomberg

고용 지표 (4월)

- 비농업 고용 증가: 177,000명 (예상치 13만 명 상회)

- 실업률: 4.2% (전월과 동일)

- 영향: 경제 둔화 우려를 완화하며 시장 낙관론에 힘을 실음

출처: WSJ

📊 투자자 심리 및 전망

- 단기 전망: 기술주 실적과 고용지표 호조로 투자심리 강세

- 중장기 우려:

- 밸류에이션 고점 논란

- 고율 관세 지속 시 기업 이익 타격 우려

- 글로벌 성장 둔화 가능성

- 전략 제안: 포트폴리오 분산 및 방어주·현금 비중 확대 권고

출처: Bloomberg

🧾 요약

2025년 5월 2일 미국 증시는 9일 연속 상승하며 강력한 상승세를 이어갔습니다. 애플과 아마존의 실적은 관세 부담과 불확실성을 내포하고 있으나, 전반적으로 시장은 고용 호조와 기술주 실적 호재에 더 주목하며 회복세를 이어가고 있습니다. 다만 무역정책과 공급망 이슈는 여전히 향후 시장 변동성의 주요 변수로 남아 있습니다.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

<영문 보고서(English Version)>

📈 Major Index Close (May 2, 2025)

| Index | Close | Change (Points) | Change (%) |

|---|---|---|---|

| S&P 500 | 5,686.67 | +82.53 | +1.47% |

| Dow Jones | 41,317.43 | +564.47 | +1.39% |

| Nasdaq Composite | 17,977.73 | +266.99 | +1.51% |

U.S. stock markets extended their rally, marking the ninth consecutive day of gains, the longest winning streak since 2004. The S&P 500 closed above its pre-tariff levels, effectively erasing the losses incurred since the escalation of the U.S.-China trade tensions in April. finance.yahoo.com+2AP News+2WSJ+2

💼 Key Earnings Reports

Apple Inc. (AAPL) – Fiscal Q2 2025

- Revenue: $95.4 billion (+5% YoY)

- Earnings Per Share (EPS): $1.65 (+8% YoY)

- Segment Highlights:

- iPhone: $46.84 billion (+2%)

- Mac: $7.95 billion (+7%)

- iPad: $6.4 billion (+15%)

- Services: $26.65 billion (+12%)

- Wearables, Home, and Accessories: $7.52 billion (-5%)

- Shareholder Returns:

- Announced a $100 billion share repurchase program

- Increased quarterly dividend by 4% to $0.26 per share

- Tariff Impact: CEO Tim Cook warned of a potential $900 million cost in the June quarter due to tariffs. To mitigate this, Apple is shifting production, with most U.S.-sold iPhones expected to be manufactured in India, and other products primarily coming from Vietnam.

- Stock Reaction: Shares fell over 4% in after-hours trading following the earnings release.

Amazon.com Inc. (AMZN) – Q1 2025

- Revenue: $155.7 billion (+9% YoY)

- Net Income: $17.1 billion ($1.59 per share), up from $10.4 billion ($0.98 per share) a year earlier

- Segment Highlights:

- Online Stores: $57.41 billion (+6%)

- Amazon Web Services (AWS): $29.27 billion (+17%)

- Advertising: $13.92 billion (+19%)

- Outlook:

- Q2 revenue forecasted between $159 billion and $164 billion

- Operating income projected between $13 billion and $17.5 billion, below analyst expectations

- Tariff Concerns: CEO Andy Jassy noted potential impacts from the 145% tariffs on Chinese imports, which affect over 50% of Amazon’s products. The company is working to maintain low prices and wide product availability by advancing inventory purchases and coordinating with third-party sellers.

- Stock Reaction: Shares declined approximately 2% in after-hours trading due to cautious guidance and tariff-related concerns.

🌐 Macroeconomic & Policy Updates

Tariff Developments

President Trump’s administration has implemented a 145% tariff on Chinese imports, impacting a significant portion of consumer goods. Companies like Apple and Amazon are adjusting their supply chains and inventory strategies to mitigate these effects.

Economic Indicators

- April Jobs Report: The U.S. economy added 177,000 jobs in April, surpassing expectations of 130,000. The unemployment rate remained steady at 4.2%. This positive data alleviated concerns over economic slowdown amid global trade uncertainties.

- Market Reaction: The strong jobs report contributed to the market rally, with investors gaining confidence in the resilience of the U.S. economy. WSJ+3theguardian.com+3schwab.com+3Investopedia

📊 Investor Sentiment & Outlook

- Short-Term: Positive momentum driven by strong tech earnings and encouraging economic data.

- Concerns:

- High equity valuations

- Ongoing trade tensions and tariff impacts

- Potential slowdown in economic growth

- Strategy: Analysts recommend portfolio diversification, noting that U.S. equities may have reached a peak.

📝 Summary

On May 2, 2025, U.S. stock markets continued their upward trajectory, buoyed by robust earnings from major tech companies and a strong April jobs report. However, the after-hours release of earnings from Apple and Amazon introduced caution, as both companies highlighted concerns over the financial impacts of newly imposed tariffs. While short-term gains persist, investors are advised to remain vigilant amid evolving economic and policy landscapes.

<This information is not investment advice, and investment decisions should be made with careful consideration. The investor is responsible for their own investment choices, and the provider of this information does not take responsibility for the investment outcomes.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<한글 보고서(Korean Version)>

📈 주요 지수 마감 현황 (2025년 5월 1일)

| 지수 | 종가 | 변동폭 (포인트) | 변동률 |

|---|---|---|---|

| S&P 500 | 5,604.14 | +35.08 | +0.63% |

| 다우 존스 산업평균지수 | 40,752.96 | +83.60 | +0.21% |

| 나스닥 종합지수 | 17,710.74 | +264.40 | +1.52% |

모든 주요 지수가 상승 마감하며 8거래일 연속 상승세를 이어갔습니다. 특히 나스닥은 기술주 강세에 힘입어 두드러진 상승을 보였습니다.

💼 주요 기업 실적 발표 및 영향

Apple (AAPL) – 2025년 2분기 실적 요약

- 총 매출: 953억 6천만 달러 (전년 대비 +5%)

- 주당순이익(EPS): $1.65 (전년 대비 +8%)

- 제품별 매출:

- iPhone: 468억 4천만 달러 (+2%)

- Mac: 79억 5천만 달러 (+7%)

- iPad: 64억 달러 (+15%)

- 서비스: 266억 5천만 달러 (+12%)

- 웨어러블/홈/액세서리: 75억 2천만 달러 (-5%)

- 주가 반응: 실적 발표 후 시간 외 거래에서 4% 이상 하락

주요 이슈:

- 관세 영향: CEO 팀 쿡은 6월 분기에 약 9억 달러의 관세 비용이 발생할 것으로 예상하며, 이를 완화하기 위해 인도와 베트남으로 생산을 이전하고 있다고 밝혔습니다.

- AI 개발 지연: Siri의 새로운 개인화 기능 출시가 다시 한 번 연기되었으며, 정확성을 높이기 위한 추가 개발 시간이 필요하다고 언급했습니다.

- 법적 문제: 에픽게임즈와의 반독점 소송에서 법원 명령 위반 판결을 받아, 형사처벌 가능성까지 제기되었습니다.

Amazon (AMZN) – 2025년 1분기 실적 요약

- 총 매출: 1,557억 달러 (전년 대비 +9%)

- 주당순이익(EPS): $1.59 (전년 $0.98)

- 부문별 매출:

- 온라인 스토어: 574억 7천만 달러 (+6%)

- AWS(클라우드): 292억 7천만 달러 (+17%)

- 광고: 139억 2천만 달러 (+19%)

- 주가 반응: 실적 발표 후 시간 외 거래에서 약 3% 하락

주요 이슈:

- 관세 불확실성: 트럼프 행정부의 145% 중국산 제품 관세로 인해 소비자 수요 둔화 우려가 있으며, 이는 2분기 실적 가이던스에 반영되어 있습니다.

- AWS 성장 둔화: 클라우드 부문 성장률이 5분기 만에 최저치를 기록하며, 투자자들의 우려를 자아냈습니다.

- AI 및 물류 투자 확대: Alexa+ 출시, 자체 AI 칩 개발, 시골 지역 배송망 확장 등으로 1분기 자본 지출이 250억 달러를 초과했습니다.

🌐 거시경제 및 정책 동향

트럼프 행정부의 관세 정책

- 배경: 4월 2일 ‘해방의 날’ 선언과 함께 전면적인 수입 관세 부과 발표

- 영향: 주요 지수 급락 및 $3조 이상의 시장 가치 증발

- 현재 상황: 90일간의 관세 유예 기간이 곧 종료 예정이며, 시장은 향후 정책 방향에 주목

경제 지표

- 1분기 GDP: 3년 만에 첫 감소 기록

- 실업수당 청구 건수: 예상보다 높은 수치

- 제조업 지표: 예상보다 양호한 결과

- 시장 반응: 혼조세를 보이며 국채 수익률 변동성 확대forbes.com+1axios.com+1

📊 투자자 동향 및 전망

- 시장 분위기: 단기적으로 기술주 중심의 반등세 지속

- 우려 사항:

- 높은 주가 밸류에이션

- 글로벌 무역 긴장 지속

- 미국 경제 성장 둔화 가능성

- 전망: 일부 전략가들은 미국 주식시장이 이미 정점을 지났다고 평가하며, 포트폴리오 다변화를 권고

🧾 요약

2025년 5월 1일 미국 증시는 기술주 실적 호조에 힘입어 상승세를 이어갔습니다. 그러나 트럼프 행정부의 관세 정책과 경제 지표의 불확실성은 여전히 시장의 주요 변수로 작용하고 있습니다. 투자자들은 단기 반등에 주목하면서도 중장기적인 리스크 관리에 신경을 기울여야 할 시점입니다.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

<영문 보고서(English Version)>

📈 Major Index Close (May 1, 2025)

| Index | Close | Change (Points) | Change (%) |

|---|---|---|---|

| S&P 500 | 5,604.14 | +35.08 | +0.63% |

| Dow Jones | 40,752.96 | +83.60 | +0.21% |

| Nasdaq Composite | 17,710.74 | +264.40 | +1.52% |

All major U.S. stock indices closed higher, extending their winning streak to eight consecutive sessions. Tech stocks led the rally, pushing the Nasdaq to notable gains.

💼 Key Earnings Reports

Apple Inc. (AAPL) – Fiscal Q2 2025

- Revenue: $95.4 billion (+5% YoY)

- Earnings Per Share (EPS): $1.65 (+8% YoY)

- Segment Highlights:

- iPhone: $46.84 billion (+2%)

- Mac: $7.95 billion (+7%)

- iPad: $6.4 billion (+15%)

- Services: $26.65 billion (+12%)

- Wearables, Home, and Accessories: $7.52 billion (-5%)

- Shareholder Returns:

- Announced a $100 billion share repurchase program

- Increased quarterly dividend by 4% to $0.26 per share

- Tariff Impact: CEO Tim Cook warned of a potential $900 million cost in the June quarter due to tariffs. To mitigate this, Apple is shifting production, with most U.S.-sold iPhones expected to be manufactured in India, and other products primarily coming from Vietnam.

- Stock Reaction: Shares fell over 4% in after-hours trading following the earnings release.Apple+4Six Colors+4The Verge+49to5Mac+1Apple+1Apple+4Investopedia+49to5Mac+4Apple+1Investopedia+1

Amazon.com Inc. (AMZN) – Q1 2025

- Revenue: $155.7 billion (+9% YoY)

- Net Income: $17.1 billion ($1.59 per share), up from $10.4 billion ($0.98 per share) a year earlier

- Segment Highlights:

- Online Stores: $57.41 billion (+6%)

- Amazon Web Services (AWS): $29.27 billion (+17%)

- Advertising: $13.92 billion (+19%)

- Outlook:

- Q2 revenue forecasted between $159 billion and $164 billion

- Operating income projected between $13 billion and $17.5 billion, below analyst expectations

- Tariff Concerns: CEO Andy Jassy noted potential impacts from the 145% tariffs on Chinese imports, which affect over 50% of Amazon’s products. The company is working to maintain low prices and wide product availability by advancing inventory purchases and coordinating with third-party sellers.

- Stock Reaction: Shares declined approximately 2% in after-hours trading due to cautious guidance and tariff-related concerns.Latest news & breaking headlines+7s2.q4cdn.com+7AP News+7s2.q4cdn.com+5Investopedia+5Latest news & breaking headlines+5Latest news & breaking headlines+1reuters.com+1finance.yahoo.com+4AP News+4reuters.com+4reuters.com+2The Guardian+2AP News+2Investopedia

🌐 Macroeconomic & Policy Updates

Tariff Developments

President Trump’s administration has implemented a 145% tariff on Chinese imports, impacting a significant portion of consumer goods. Companies like Apple and Amazon are adjusting their supply chains and inventory strategies to mitigate these effects. AP News

Economic Indicators

- Q1 GDP: Contracted at a 0.3% annualized rate, marking the first decline in three years.

- Jobless Claims: Higher than expected, indicating potential softening in the labor market.

- Manufacturing Activity: Exceeded expectations, suggesting resilience in the sector.The Guardian

📊 Investor Sentiment & Outlook

- Short-Term: Positive momentum driven by strong tech earnings.

- Concerns:

- High equity valuations

- Ongoing trade tensions and tariff impacts

- Potential slowdown in economic growth

- Strategy: Analysts recommend portfolio diversification, noting that U.S. equities may have reached a peak. The Guardian

📝 Summary

On May 1, 2025, U.S. stock markets continued their upward trajectory, buoyed by robust earnings from major tech companies. However, the after-hours release of earnings from Apple and Amazon introduced caution, as both companies highlighted concerns over the financial impacts of newly imposed tariffs. While short-term gains persist, investors are advised to remain vigilant amid evolving economic and policy landscapes.

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<한글 보고서(Korean Version)>

📈 주요 주가지수 마감 현황

2025년 4월 30일(수), 미국 주식시장은 혼조세로 마감했습니다. 1분기 국내총생산(GDP) 감소 소식으로 장 초반 하락했으나, 장 후반 반등하며 일부 지수는 상승세로 전환했습니다.

- S&P 500: 5,569.06 (+0.15%)

- 다우존스 산업평균지수: 40,669.36 (+0.35%)

- 나스닥 종합지수: 17,446.34 (−0.09%)

- 러셀 2000: 1,964.12 (−0.6%)

S&P 500과 다우존스 지수는 각각 7일 연속 상승하며 4월을 마감했으나, 월간 기준으로는 각각 0.8%, 3.2% 하락했습니다. 나스닥은 4월 한 달간 0.9% 상승하며 2개월 연속 하락세를 끊었습니다.

🏢 주요 기업 실적 발표

마이크로소프트(MSFT)

- 1분기 주당순이익(EPS)은 $2.45로 예상치를 상회했습니다.

- 클라우드 서비스 부문의 강력한 성장으로 매출이 전년 대비 8% 증가했습니다.

메타 플랫폼스(META)

- EPS는 $3.20으로 시장 예상치를 초과했습니다.

- 광고 수익이 12% 증가하며 플랫폼 전반에서 강한 수요를 보였습니다.

퀄컴(QCOM)

- EPS는 $1.90으로 시장 기대에 부합했습니다.

- 스마트폰 시장의 부진을 자동차용 칩 판매 증가로 상쇄하며 매출을 안정적으로 유지했습니다.

📉 경제 지표 및 동향

국내총생산(GDP)

미국 상무부 경제분석국(BEA)의 발표에 따르면, 2025년 1분기 실질 GDP는 연율 기준 0.3% 감소하여 2022년 이후 처음으로 마이너스를 기록했습니다. 이는 트럼프 대통령의 새로운 관세 정책 시행 전 기업들이 수입을 앞당기면서 수입이 급증한 것이 주요 원인으로 지목됩니다.

인플레이션(PCE 지수)

3월 개인소비지출(PCE) 가격지수는 전월 대비 변동이 없었으며, 전년 동월 대비로는 2.3% 상승했습니다. 식품과 에너지를 제외한 근원 PCE 지수는 전년 대비 2.6% 상승하여 연준의 목표치에 근접했습니다.

소비자 신뢰지수

컨퍼런스보드의 발표에 따르면, 4월 소비자 신뢰지수는 86.0으로 전월 대비 7.9포인트 하락하며 2020년 5월 이후 최저치를 기록했습니다. 특히 향후 6개월에 대한 기대를 나타내는 기대지수는 54.4로 2011년 10월 이후 최저 수준으로 떨어졌습니다.

🧭 시장 전망 및 투자 전략

1분기 GDP 감소와 소비자 신뢰지수 하락은 미국 경제의 불확실성을 높이고 있습니다. 트럼프 대통령은 이번 경제 둔화가 전임 바이든 행정부의 영향이라고 주장하며, 자신의 관세 정책은 장기적으로 긍정적인 효과를 가져올 것이라고 강조했습니다.

경제 전문가들은 현재의 경제 지표들이 경기 침체의 초기 신호일 수 있다고 경고하며, 투자자들에게 방어적인 포트폴리오 구성과 신중한 투자 전략을 권장하고 있습니다. 특히, 향후 발표될 고용 지표와 연준의 금리 정책에 대한 주의 깊은 관찰이 필요합니다.

<영문 보고서(English Version)>

📈 Market Overview

On April 30, 2025, U.S. stock markets exhibited mixed results as investors grappled with economic contraction concerns and ongoing trade tensions.

- S&P 500: 5,569.06 (+0.1%)

- Dow Jones Industrial Average: 40,669.36 (+0.3%)

- Nasdaq Composite: 17,446.34 (−0.1%)

- Russell 2000: 1,964.12 (−0.6%)AP News

Despite early losses prompted by a report indicating economic contraction, the S&P 500 achieved its seventh consecutive gain, and the Dow Jones marked its longest winning streak in nearly a year.

🏢 Corporate Earnings Highlights

Microsoft (MSFT)

- Reported earnings per share (EPS) of $2.45, surpassing analysts’ expectations.

- Revenue increased by 8% year-over-year, driven by strong cloud services performance.

Meta Platforms (META)

- Announced EPS of $3.20, exceeding forecasts.

- Advertising revenue grew by 12%, reflecting robust demand across platforms.

Qualcomm (QCOM)

- Posted EPS of $1.90, aligning with market expectations.

- Revenue remained stable, with growth in automotive chip sales offsetting smartphone market softness.

📉 Economic Indicators

Gross Domestic Product (GDP)

- The U.S. economy contracted at an annual rate of 0.3% in Q1 2025, marking the first decline since early 2022.

- The contraction was primarily due to a surge in imports ahead of new tariffs, widening the trade deficit.

Inflation

- The core Personal Consumption Expenditures (PCE) price index rose 2.6% year-over-year in March, indicating persistent inflationary pressures.

Consumer Confidence

- The Conference Board’s Consumer Confidence Index fell by 7.9 points to 86.0 in April, the lowest level since May 2020.

🧭 Market Outlook

While corporate earnings have provided some support to the markets, the combination of economic contraction, inflation concerns, and declining consumer confidence suggests a cautious outlook. Investors are advised to monitor developments in trade policies and economic indicators closely.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<한글 보고서(Korean Version)>

2025년 4월 29일 미국 주식시장은 변동성이 큰 가운데 상승 마감하였습니다. 이는 기업 실적 발표와 무역 정책 변화에 대한 투자자들의 반응에 따른 것으로 보입니다.

📊 주요 지수 마감 현황 (2025년 4월 29일)

- S&P 500: 5,560.83 (+0.6%)

- 다우 존스 산업평균지수: 40,527.62 (+0.7%)

- 나스닥 종합지수: 17,461.32 (+0.5%)n

이날 상승은 4월 초 도널드 트럼프 대통령의 전면적 관세 부과로 인한 급락 이후의 회복세를 반영합니다. 그러나 시장은 여전히 불안정한 상태입니다.

🏢 주요 기업 실적 및 반응

- UPS: 1분기 실적은 예상치를 상회했으나, 연간 가이던스를 철회하고 20,000명 감원을 발표하여 주가는 하락했습니다.

- 제너럴 모터스(GM): 예상보다 높은 실적을 발표했지만, 관세 불확실성으로 연간 전망을 철회하여 주가는 하락했습니다.

- 코카콜라: 실적이 예상치를 상회했으며, 관세 영향이 제한적이라고 밝혔습니다.

📉 경제 지표 및 시장 전망

- GDP: 2025년 1분기 미국 GDP는 0.3% 감소하여 경기 침체 우려를 키웠습니다.

- 인플레이션: 핵심 PCE 물가지수는 3.5% 상승하여 연준의 금리 인하 여지를 제한하고 있습니다.

- 소비자 신뢰지수: 2020년 5월 이후 최저치를 기록하며 소비 심리 위축을 나타냈습니다.

골드만삭스는 시장이 아직 바닥을 치지 않았으며, 경기 침체가 지속될 경우 하반기까지 하락세가 이어질 수 있다고 전망했습니다.

🧭 투자자 대응 전략

시장 전문가들은 현재의 반등을 약세장 속 일시적 회복으로 보고 있습니다. 불확실한 무역 정책과 경제 지표 악화로 인해 방어적인 투자 전략이 권장됩니다. 특히, 기술주와 같은 고평가 종목에 대한 주의가 필요하며, 현금 비중을 높이는 것이 바람직할 수 있습니다.

전반적으로, 4월 29일 미국 주식시장은 단기 반등을 보였으나, 근본적인 불확실성은 여전히 존재합니다. 투자자들은 경제 지표와 정책 변화를 면밀히 주시하며 신중한 접근이 요구됩니다.

<영문 보고서(English Version)>

📈 Market Overview

On April 29, 2025, U.S. stock markets closed higher, buoyed by stronger-than-expected corporate earnings despite ongoing concerns about tariffs and economic indicators.

- S&P 500: 5,560.83 (+0.6%)

- Dow Jones Industrial Average: 40,527.62 (+0.7%)

- Nasdaq Composite: 17,461.32 (+0.5%)

- Russell 2000: 1,976.52 (+0.6%)

This marks the sixth consecutive gain for the S&P 500, though all major indexes remain down year-to-date, reflecting broader economic concerns and market volatility.

🏢 Corporate Earnings Highlights

UPS (NYSE: UPS)

- Reported Q1 2025 consolidated revenues of $21.5 billion, a 0.7% decrease from Q1 2024.

- Adjusted diluted earnings per share were $1.49, 4.2% above the same period in 2024.

- Announced plans to cut approximately 20,000 jobs and close 73 buildings by the end of June, aiming to reduce costs amid declining volumes and tariff impacts.

General Motors (NYSE: GM)

- Q1 net income decreased 6.6% to $2.8 billion.

- Withdrew its 2025 profit guidance and suspended a $4 billion share buyback program due to uncertainty over U.S. auto tariffs.

Coca-Cola (NYSE: KO)

- Q1 revenue slightly declined to $11.22 billion, beating expectations.

- Adjusted earnings per share were $0.73, surpassing estimates.

- The company noted that tariffs could impact consumer sentiment but expressed confidence in managing the challenges.

📉 Economic Indicators

Gross Domestic Product (GDP)

- The U.S. economy contracted at an annual rate of 0.3% in Q1 2025, marking the first decline since early 2022.

- The contraction was primarily due to a surge in imports ahead of new tariffs and a decrease in government spending. WSJ+9The Washington Post+9theguardian.com+9

Inflation

- The core Personal Consumption Expenditures (PCE) price index rose 2.6% year-over-year in March, down from 3.0% in February, indicating a slight easing in inflation pressures. FXStreet+2Wolf Street+2Investing.com+2

Consumer Confidence

- The Conference Board’s Consumer Confidence Index fell by 7.9 points to 86.0 in April, the lowest level since May 2020, reflecting growing pessimism about the economy and labor market due to tariffs. Upi+5Bloomberg+5The Conference Board+5

🧭 Market Outlook

While corporate earnings have provided some support to the markets, the combination of economic contraction, inflation concerns, and declining consumer confidence suggests a cautious outlook. Investors are advised to monitor developments in trade policies and economic indicators closely.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<한글 보고서(Korean Version)>

2025년 4월 28일(월요일) 미국 주식시장은 혼조세로 마감되었습니다. 투자자들은 주요 기술기업들의 실적 발표와 1분기 경제 지표 발표를 앞두고 관망세를 보였으며, 최근 도널드 트럼프 대통령의 관세 정책으로 인한 불확실성도 시장에 영향을 미쳤습니다.

📊 주요 지수 마감 현황

- S&P 500: 5,528.75 (+3.54포인트, +0.1%)

- 다우존스 산업평균지수: 40,227.59 (+114.09포인트, +0.3%)

- 나스닥 종합지수: 17,366.13 (-16.81포인트, -0.1%)

- 러셀 2000: 1,965.55 (+7.93포인트, +0.4%)

S&P 500과 다우존스 지수는 각각 5일 연속 상승세를 이어갔으며, 이는 2024년 11월 이후 가장 긴 상승 기록입니다. 반면, 기술주 중심의 나스닥 지수는 소폭 하락하며 혼조세를 보였습니다.

🏢 업종 및 주요 종목 동향

- 헬스케어: 애브비(AbbVie)는 1분기 실적이 예상을 상회하고 연간 수익 전망을 상향 조정하면서 주가가 3.4% 상승했습니다. 길리어드 사이언스(Gilead Sciences)도 HIV 및 간 질환 치료제 판매 호조로 3.1% 반등했습니다.I

- 소비재: 콜게이트-팜올리브(Colgate-Palmolive)는 양호한 분기 실적에도 불구하고 관세 우려로 연간 전망을 하향 조정하면서 주가가 3.1% 하락했습니다.

- 기술주: 화웨이의 AI 칩 개발 소식으로 인해 엔비디아(Nvidia)는 2.1% 하락했습니다.

🌐 시장 배경 및 경제 지표

4월 2일 도널드 트럼프 대통령이 발표한 전면적인 수입 관세 정책(일명 ‘해방의 날’) 이후, 미국 주식시장은 큰 폭의 하락을 겪었습니다. S&P 500은 2일간 10.5% 하락했으며, 다우존스 지수는 4,580포인트 이상 하락했습니다. 이러한 조치는 글로벌 무역 긴장을 고조시키고 투자자들의 신뢰를 약화시켰습니다.

<영문 보고서(English Version)>

📊 Major Index Performance

- S&P 500: 5,528.75 (+3.54 points, +0.1%)

- Dow Jones Industrial Average: 40,227.59 (+114.09 points, +0.3%)

- Nasdaq Composite: 17,366.13 (-16.81 points, -0.1%)

- Russell 2000: 1,965.55 (+7.93 points, +0.4%)

The S&P 500 and the Dow Jones Industrial Average both posted their fifth consecutive day of gains, marking the longest winning streak since November 2024. Meanwhile, the Nasdaq closed slightly lower, reflecting a mixed performance across major indices.

🏢 Sector and Major Stock Movements

- Healthcare:

AbbVie gained 3.4% after posting stronger-than-expected Q1 earnings and raising its full-year guidance.

Gilead Sciences rose 3.1%, supported by strong sales of HIV and liver disease treatments. - Consumer Goods:

Colgate-Palmolive dropped 3.1% despite beating earnings estimates, as it lowered its full-year outlook citing concerns over rising tariffs. - Technology:

Nvidia fell 2.1% after reports that Huawei is accelerating its development of AI chips.

🌐 Market Context and Economic Indicators

Following President Donald Trump’s announcement of sweeping import tariffs on April 2 (“Liberation Day”), the U.S. stock market experienced a sharp downturn.

- The S&P 500 plunged 10.5% over two days.

- The Dow Jones Industrial Average lost over 4,580 points during the same period.

This heightened trade tensions globally and significantly dented investor confidence.

Looking ahead, investors are focused on major upcoming events this week, including:

- Earnings releases from tech giants such as Apple, Amazon, Microsoft, and Meta Platforms.

- The first-quarter GDP growth report.

- April employment data.

These factors are expected to inject additional volatility into the market.

📈 Conclusion and Outlook

The U.S. stock market closed mixed on April 28, 2025, as investors adopted a cautious stance ahead of key earnings and economic reports.

While the recent tariff announcements have added significant uncertainty, the market’s near-term direction will likely be determined by upcoming corporate earnings results and macroeconomic data.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

<한글 보고서(Korean Version)>

2025년 4월 25일 미국 주식시장은 기술주 중심의 상승세를 보이며 4일 연속 상승 마감했습니다. 이는 4월 초 도널드 트럼프 대통령의 전면적인 관세 발표로 인한 급락 이후의 반등 흐름으로, 시장은 무역 긴장 완화 기대와 주요 기술기업들의 실적 호조에 힘입어 회복세를 이어갔습니다.

📈 주요 지수 마감 현황 (2025년 4월 25일)

- S&P 500: 5,525.21 (+0.7%)

- 나스닥 종합지수: 17,382.94 (+1.3%)

- 다우존스 산업평균지수: 40,113.50 (+0.05%)

이번 주간 기준으로는 나스닥이 6.7%, S&P 500이 4.6%, 다우가 2.5% 상승하며 강한 회복세를 보였습니다.

🔍 시장 주요 동향 및 이슈

1. 기술주 주도 상승

알파벳(구글)은 1분기 순이익이 50% 증가하고 700억 달러 규모의 자사주 매입을 발표하며 주가가 1.7% 상승했습니다. 엔비디아는 4.3% 상승하며 나스닥 상승을 견인했습니다. 반면, 인텔은 실적 부진과 비용 우려로 6.7% 하락했습니다.

2. 무역 긴장 완화 기대

트럼프 대통령은 중국 및 일본과의 무역 협상이 진행 중이라고 밝혔으나, 중국은 이를 부인했습니다. 그럼에도 불구하고 시장은 관세 완화 가능성에 대한 기대감으로 상승세를 보였습니다.

3. 소비자 심리 악화

미시간대 소비자 심리지수에 따르면, 소비자들의 경제 기대치는 1월 이후 32% 급락하여 1990년대 이후 최저치를 기록했습니다. 이는 무역 전쟁에 따른 인플레이션 우려와 경제 둔화 전망 때문입니다.

🧾 기업 실적 요약

- 알파벳(GOOGL): 1분기 매출 902억 3천만 달러, EPS 2.81달러로 예상 상회. AI 및 클라우드 부문 성장 지속.

- 서비스나우(ServiceNow), SAP: 예상치 상회하는 실적 발표.

- 인텔(Intel): 실적 부진과 비용 우려로 주가 하락.

- 테슬라(Tesla): 재무 실적은 부진했으나, 일론 머스크의 정치적 활동 축소 및 로보택시 계획 발표로 주가 상승.

📊 투자자 심리 및 전망

시장 변동성에도 불구하고, 뱅가드에 따르면 401(k) 계좌 보유자의 약 97%가 중순까지 거래를 하지 않아 장기 투자 성향을 보였습니다.

일부 월가 전략가들은 현재의 비관론이 과도하다고 판단하며, 강한 기업 실적과 견고한 노동 시장을 바탕으로 주식 매수 기회로 보고 있습니다.

🔮 향후 주목할 이벤트

- 주요 기술기업 실적 발표: 애플, 마이크로소프트, 아마존, 메타 등의 실적 발표 예정.

- 경제 지표 발표: 1분기 GDP 성장률, PCE 인플레이션 지수, 4월 고용보고서 등이 예정되어 있어 시장에 영향을 줄 수 있습니다.

전반적으로 4월 25일의 미국 주식시장은 기술주 중심의 상승세와 무역 긴장 완화 기대감으로 긍정적인 흐름을 보였으나, 소비자 심리 악화와 무역 정책의 불확실성 등 여전히 주의가 필요한 요소들이 존재합니다.

<영문 보고서(English Version)>

🔹 Major Index Performance (Closing – April 25, 2025)

- S&P 500: 5,525.21 (+0.7%)

- Nasdaq Composite: 17,382.94 (+1.3%)

- Dow Jones Industrial Average: 40,113.50 (+0.05%)

For the week, the Nasdaq rose 6.7%, the S&P 500 gained 4.6%, and the Dow added 2.5%, continuing a strong recovery after sharp declines earlier in April.

(Source: AP News)

🔹 Key Market Drivers

1. Tech-Led Rally

- Alphabet (Google) surged 1.7% after posting a 50% increase in quarterly profit and announcing a $70 billion stock buyback program.

- Nvidia jumped 4.3%, helping to lift the Nasdaq.

- Intel plunged 6.7% on disappointing earnings and cost concerns. (Source: AP News)

2. Hopes for Easing Trade Tensions

- President Trump stated that trade negotiations with China and Japan were progressing, though China denied any progress.

- Markets reacted positively, fueled by optimism for potential tariff rollbacks. (Source: Reuters)

3. Consumer Sentiment Weakness

- The University of Michigan’s consumer sentiment index showed a sharp 32% drop in economic expectations since January, marking the lowest reading since the 1990s.

- Concerns over inflation and potential economic slowdown from the trade war were cited. (Source: The Guardian)

🔹 Earnings Highlights

- Alphabet (GOOGL): Q1 revenue of $90.23 billion, EPS of $2.81 – both beating expectations. Strong growth in AI and cloud services divisions.

- ServiceNow and SAP: Reported earnings above forecasts.

- Intel: Missed earnings expectations, citing rising costs.

- Tesla: Despite weaker financial results, shares rose after Elon Musk announced reduced political activities and plans for a “robotaxi” service.

(Source: Investors.com)

🔹 Investor Sentiment and Outlook

- Despite market turbulence, around 97% of Vanguard 401(k) holders made no changes to their accounts, indicating strong long-term investment behavior. (Source: Washington Post)

- Some Wall Street strategists view the recent market pessimism as overblown, suggesting that strong corporate earnings and a robust labor market present opportunities to “buy the dip.” (Source: Business Insider)

🔹 Upcoming Catalysts

- Big Tech Earnings: Upcoming reports from Apple, Microsoft, Amazon, and Meta will likely influence the market direction.

- Key Economic Data: 1Q GDP growth rate, PCE inflation index, and the April jobs report are scheduled for release.

🔵 Conclusion

On April 25, 2025, the U.S. stock market extended its recovery rally, led by tech giants and optimism over potential easing of trade tensions. However, risks remain as consumer sentiment weakens and trade policy uncertainty persists.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

🔹 주요 지수 마감 현황 (2025년 4월 24일)

- S&P 500: 5,484.77 (+2.0%)

- 나스닥 종합지수: 17,166.04 (+2.7%)

- 다우존스 산업평균지수: 40,093.40 (+1.2%)

- 러셀 2000 소형주 지수: 1,957.59 (+2.0%)

👉 3거래일 연속 상승세를 기록했으며, 이는 강한 기업 실적 발표와 미중 무역 긴장 완화 기대감이 시장을 이끈 결과입니다.

(출처: AP News)

🔹 시장 주요 동향

1. 기술주 주도 상승

- 알파벳(Google 모기업):

1분기 매출 902억 달러, 주당순이익(EPS) 2.81달러로 시장 예상치를 크게 상회했습니다. 특히 인공지능(AI) 사업 부문, ‘Gemini 2.5’ 출시 등이 실적 호조에 기여했습니다.

(출처: Business Insider) - ServiceNow:

예상치를 웃도는 수익을 기록하며, 엔터프라이즈 소프트웨어 수요가 여전히 견조함을 입증했습니다.

(출처: AP News)

2. 무역 긴장 완화 기대

- 트럼프 대통령은 중국 제품에 대한 관세를 일부 철회할 가능성을 언급했고, 미국 재무장관 스콧 베센트도 미중 관계 개선 가능성을 언급했습니다.

- 하지만 중국 측은 공식적으로 “현재 무역 협상은 없다”고 부인해 시장에 불확실성을 남겼습니다.

(출처: New York Post)

3. 인텔 실적 부진

- 인텔(Intel):

1분기 매출 126억 7천만 달러로 예상치를 소폭 상회했지만, 2분기 매출 전망을 112억~124억 달러로 제시해 시장 기대에 못 미쳤습니다.

AI 칩 시장에서의 경쟁 심화와 거시경제 불확실성이 주요 원인으로 지적되었습니다.

(출처: The Times)

🔹 주간 시장 수익률

- S&P 500: +3.8%

- 나스닥 종합지수: +5.4%

- 다우존스 산업평균지수: +2.4%

- 러셀 2000: +4.1%

👉 다만, 2025년 들어서는 여전히 연초 대비 마이너스 수익률을 기록하고 있어 변동성이 큰 장세가 이어지고 있습니다.

(출처: AP News)

🔹 향후 주목할 이벤트

- 애플, 마이크로소프트, 아마존, 메타 등 빅테크 기업들의 실적 발표 예정

- 미국 1분기 GDP 성장률, 4월 고용보고서 발표 예정

- 미중 무역 관련 발언 및 정책 변화 가능성

👉 시장은 경제지표 및 기업 실적 결과에 따라 방향성을 결정할 가능성이 큽니다.

🔵 결론

2025년 4월 24일, 미국 주식시장은 기술주를 중심으로 강한 반등을 이어갔으며, 무역 긴장 완화 기대와 주요 기업들의 긍정적인 실적 발표가 상승세를 이끌었습니다. 다만, 인텔과 같이 일부 기업들은 매출 전망 부진을 보였고, 미중 관계 불확실성도 여전히 시장 리스크로 남아 있습니다.

📊 Major Index Performance (April 24, 2025)

- S&P 500: 5,484.77 (+2.0%)

- Nasdaq Composite: 17,166.04 (+2.7%)

- Dow Jones Industrial Average: 40,093.40 (+1.2%)

- Russell 2000: 1,957.59 (+2.0%)Bloomberg.com+2AP News+2Reuters+2

This marked the third consecutive day of gains, driven by robust earnings reports and optimism over potential easing of U.S.-China trade tensions. AP News

🧠 Key Market Drivers

1. Technology Sector Rally

- Alphabet (GOOGL): Reported Q1 revenue of $90.2 billion and EPS of $2.81, surpassing analyst expectations. The company’s AI initiatives, including the rollout of Gemini 2.5, contributed to the strong performance. Business Insider

- ServiceNow: Delivered stronger-than-expected profits, boosting investor confidence in enterprise software demand. AP News

2. Trade Tension Developments

President Trump’s indications of potential tariff reductions on Chinese goods, coupled with statements from Treasury Secretary Scott Bessent about improving relations with China, fueled investor optimism. However, China denied ongoing trade talks, adding complexity to the situation. New York Post

3. Intel’s Mixed Earnings Report

- Intel (INTC): Posted Q1 revenue of $12.67 billion, slightly exceeding expectations. However, the company forecasted Q2 revenue between $11.2 billion and $12.4 billion, below analyst estimates, citing macroeconomic uncertainties and challenges in the AI chip market. Seeking Alpha+2Latest news & breaking headlines+2Investopedia+2

📈 Weekly Performance Overview

- S&P 500: +3.8%

- Nasdaq Composite: +5.4%

- Dow Jones Industrial Average: +2.4%

- Russell 2000: +4.1%Seeking AlphaAP News

Despite the recent rally, all major indexes remained negative year-to-date, reflecting ongoing market volatility. AP News

🔮 Outlook

Investors are closely monitoring upcoming earnings reports from major tech firms, including Apple, Microsoft, Amazon, and Meta, as well as key economic indicators such as Q1 GDP growth and April employment data. The market remains sensitive to developments in trade policies and macroeconomic conditions.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

1. 요약

2025년 4월 23일 미국 증시는 도널드 트럼프 대통령의 연준(Fed) 의장 해임 철회 및 중국과의 무역 긴장 완화 시사에 힘입어 상승 마감했습니다. 이는 전일의 반등세를 이어가는 모습으로, 투자자들의 불안감이 다소 해소된 결과로 풀이됩니다.

2. 2025년 4월 23일 미국 증시 마감 현황

- S&P 500: 5,375.86포인트 (+1.7%, +88.10포인트)

- 다우존스 산업평균지수: 39,606.57포인트 (+1.1%, +419.59포인트)

- 나스닥 종합지수: 16,708.05포인트 (+2.5%, +407.63포인트)

- 러셀 2000: 1,919.14포인트 (+1.5%, +28.86포인트)

이날 상승은 트럼프 대통령이 연준 의장 제롬 파월을 해임할 의사가 없다고 밝히고, 중국에 대한 관세를 “상당히 낮출 것”이라고 언급한 데 따른 것입니다. 이러한 발언은 연준의 독립성에 대한 우려를 완화하고, 미중 무역 긴장 완화에 대한 기대감을 높였습니다.

3. 주요 상승 요인 및 종목

- 기술주 강세: 나스닥 지수가 2.5% 상승하며 기술주가 시장 상승을 주도했습니다.

- 보잉(Boeing): 예상치를 상회하는 실적 발표로 투자자들의 신뢰를 얻었습니다.

- 테슬라(Tesla): 분기 순이익 감소에도 불구하고 주가가 상승했습니다.

4. 시장 배경 및 정책 요인

- 무역 긴장 완화 기대: 트럼프 대통령은 중국과의 무역 갈등 완화 가능성을 시사하며, 관세를 “상당히 낮출 것”이라고 언급했습니다. 스콧 베센트 재무장관도 미중 간 관세 대립이 지속 가능하지 않다고 밝혔습니다.

- 연준 독립성 우려 완화: 트럼프 대통령이 연준 의장 해임 계획이 없다고 밝히면서, 연준의 독립성에 대한 우려가 완화되었습니다.

5. 연초 대비 주요 지수 변동률 (2025년 4월 23일 기준)

- S&P 500: -8.6%

- 다우존스 산업평균지수: -6.9%

- 나스닥 종합지수: -13.5%

- 러셀 2000: -13.9%

6. 요약 및 전망

2025년 4월 23일 미국 증시는 트럼프 대통령의 연준 의장 해임 철회 및 중국과의 무역 긴장 완화 시사에 힘입어 상승 마감했습니다. 이는 투자자들의 불안감을 다소 해소하며, 시장에 긍정적인 영향을 미쳤습니다. 그러나 연준의 독립성에 대한 우려와 무역 정책의 불확실성이 여전히 상존하므로, 향후 시장은 변동성을 지속할 가능성이 있습니다. 투자자들은 이러한 요인들을 주의 깊게 관찰하며 신중한 투자 전략을 수립하는 것이 중요합니다.

1. Summary

On April 23, 2025, U.S. stock markets closed higher, continuing the previous day’s rebound. The gains were driven by President Donald Trump’s announcement that he has no intention to fire Federal Reserve Chair Jerome Powell and his indication of a potential reduction in tariffs on Chinese imports. These statements eased investor concerns regarding the Fed’s independence and U.S.-China trade tensions.

2. U.S. Stock Market Closing Data (April 23, 2025)

- S&P 500: 5,375.86 (+1.7%, +88.10 points)

- Dow Jones Industrial Average: 39,606.57 (+1.1%, +419.59 points)

- Nasdaq Composite: 16,708.05 (+2.5%, +407.63 points)

- Russell 2000: 1,919.14 (+1.5%, +28.86 points)

3. Key Drivers and Notable Stocks

- Tech Sector Strength: The Nasdaq Composite rose by 2.5%, leading the market gains.

- Boeing: Reported better-than-expected earnings, boosting investor confidence.

- Tesla: Despite a significant drop in quarterly profits, the stock rallied.

4. Market Context and Policy Factors

Federal Reserve Independence: Trump clarified that he has no plans to dismiss Fed Chair Jerome Powell, alleviating concerns about the central bank’s independence..

Trade Tension Easing: President Trump signaled a willingness to de-escalate the trade war with China, stating that tariffs could be “substantially lower.” Treasury Secretary Scott Bessent also mentioned that high tariffs between the U.S. and China are unsustainable.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

1. 요약

2025년 4월 22일 미국 증시는 전일의 급락을 만회하며 강한 반등세를 보였습니다. 이는 긍정적인 기업 실적 발표와 미중 무역 긴장 완화 기대감, 그리고 연방준비제도(Fed)에 대한 정치적 압력이 일시적으로 완화된 데 기인합니다.

2. 주요 지수 마감 현황 (2025년 4월 22일)

- S&P 500: 5,287.76포인트 (+2.5%)

- 다우존스 산업평균지수: 39,186.98포인트 (+2.7%)

- 나스닥 종합지수: 16,300.42포인트 (+2.7%)

- 러셀 2000: 1,890.28포인트 (+2.7%)

이날 상승은 전일 급락에 대한 기술적 반등과 함께, 주요 기업들의 실적 호조가 투자 심리를 개선시킨 결과입니다.

3. 주요 상승 종목 및 섹터

- Equifax (EFX): 1분기 실적 호조와 자사주 매입 계획 발표로 주가가 13.8% 상승했습니다.

- 3M (MMM): 예상치를 상회하는 실적 발표로 8.1% 상승하며 다우 지수 상승을 견인했습니다.

- Tesla (TSLA): 실적 발표를 앞두고 4.6% 상승했습니다.

- Nvidia, Apple, Meta: 각각 3% 이상 상승하며 기술주 전반의 회복세를 이끌었습니다.

또한, First Solar는 미국의 태양광 패널에 대한 신규 관세 발표로 10.5% 상승했습니다.

4. 시장 배경 및 정책 요인

최근 시장의 변동성은 도널드 트럼프 대통령의 연준 비판과 무역 정책에 대한 불확실성에서 비롯되었습니다. 그러나 이날은 트럼프 대통령이 연준 의장 제롬 파월에 대한 추가 비판을 자제하고, 미중 간 무역 갈등에 대한 완화 가능성을 시사하면서 투자자들의 불안이 다소 해소되었습니다.

또한, 재무장관 스콧 베센트는 미중 간 관세 대립이 지속 가능하지 않으며, 협상이 이루어질 가능성이 높다고 언급하여 시장에 긍정적인 신호를 보냈습니다.

5. 연초 대비 지수 변동률

- S&P 500: -10.1%

- 다우존스 산업평균지수: -7.9%

- 나스닥 종합지수: -15.6%

- 러셀 2000: -15.2%

연초 대비 주요 지수들은 여전히 하락세를 보이고 있으나, 이날의 반등은 시장의 회복 가능성을 보여주는 긍정적인 신호로 해석됩니다.

6. 요약 및 전망

2025년 4월 22일의 미국 증시 반등은 기업 실적 호조와 정책 불확실성 완화 기대감이 결합된 결과입니다. 그러나 연준의 독립성에 대한 우려와 무역 정책의 불확실성이 여전히 상존하므로, 향후 시장은 변동성을 지속할 가능성이 있습니다. 투자자들은 이러한 요인들을 주의 깊게 관찰하며 신중한 투자 전략을 수립하는 것이 중요합니다.

📊 U.S. Stock Market Daily Report

1. Major Index Performance (April 22, 2025)

- S&P 500: 5,287.76 (+2.5%)

- Dow Jones Industrial Average: 39,186.98 (+2.7%)

- Nasdaq Composite: 16,300.42 (+2.7%)

- Russell 2000: 1,890.28 (+2.7%)

Markets rebounded strongly after the previous day’s sharp losses, fueled by positive earnings reports, optimism around U.S.–China trade negotiations, and a temporary pause in political pressure on the Federal Reserve.

(Source: AP News)

2. Top Gainers and Leading Sectors

- Equifax (EFX) surged 13.8% after strong Q1 earnings and a share buyback announcement.

- 3M (MMM) rose 8.1%, beating earnings expectations and helping lift the Dow.

- Tesla (TSLA) gained 4.6% ahead of earnings release.

- Nvidia, Apple, Meta each advanced over 3%, leading a tech sector rebound.

- First Solar jumped 10.5% amid news of new U.S. tariffs on solar panel imports.

(Source: Investopedia, AP News)

3. Market Drivers & Policy Outlook

Recent volatility had stemmed from President Donald Trump’s criticism of Fed policy and ongoing trade tensions. However, sentiment improved as Trump held back on further criticism of Fed Chair Jerome Powell and hinted at possible progress with China on trade.

Treasury Secretary Scott Bessent also reassured markets by stating that continued tariff conflict with China was “unsustainable” and that negotiations were likely.

(Source: Reuters)

4. Year-to-Date Performance

- S&P 500: –10.1%

- Dow Jones: –7.9%

- Nasdaq: –15.6%

- Russell 2000: –15.2%

Despite today’s rally, major indexes remain in negative territory for the year, though the bounce suggests signs of possible stabilization.

(Source: AP News)

5. Summary & Outlook

The sharp rebound on April 22 signals investor relief over strong corporate earnings and waning political and trade uncertainty. However, risks remain—including doubts about Fed independence and long-term trade policy clarity.

Markets may continue to experience volatility, and investors should stay cautious while watching for signals from earnings releases, Fed communications, and U.S.–China trade developments.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

1. 주요 지수 마감 현황

| 지수 | 마감 지수 | 등락폭 | 등락률 |

|---|---|---|---|

| 다우존스 산업평균지수 | 38,170.41 | -971.82 | -2.48% |

| S&P 500 | 5,158.20 | -124.50 | -2.36% |

| 나스닥 종합지수 | 15,870.90 | -415.55 | -2.55% |

모든 주요 지수가 2% 이상 하락하며, 기술주 중심의 나스닥이 가장 큰 하락폭을 기록했습니다.

2. 하락 요인 분석

▪ 트럼프 대통령의 연준 비판

도널드 트럼프 대통령은 연준 의장 제롬 파월을 향해 “Mr. Too Late, a major loser”라고 비난하며 즉각적인 금리 인하를 촉구했습니다. 이러한 발언은 연준의 독립성에 대한 우려를 증폭시켰습니다.

▪ 미중 무역 긴장 고조

중국은 미국과의 무역 협상에 대한 경고를 발하며, 미국의 보호무역 정책에 대한 반발을 나타냈습니다. 이는 글로벌 무역 불확실성을 증가시켰습니다.

▪ 기술주 중심의 매도세

“Magnificent Seven”으로 불리는 대형 기술주들이 하락세를 주도했습니다. 특히, 테슬라는 생산 지연 소식으로 5.8% 하락했고, 엔비디아는 화웨이의 AI 칩 출하 소식으로 4.5% 하락했습니다.

3. 섹터별 동향

S&P 500의 11개 섹터 모두 하락 마감했습니다.

- 가장 큰 하락: 소비재 및 기술 섹터

- 상대적 선방: 필수소비재 및 부동산 섹터

4. 주요 종목 등락

▪ 상승 종목

- Discover Financial Services: +3.6% (Capital One과의 합병 승인)

- Fidelity National Information Services: +2.4% (시티그룹의 주식 등급 상향)

- Netflix: +1.5% (강력한 실적 발표 및 분석가들의 목표가 상향)

▪ 하락 종목

- Universal Health Services: -10.2% (Medicaid 관련 수익 감소 우려)

- Blackstone: -7.8% (자산 매각 둔화 전망)

- Vistra: -7.7% (에너지 부문 예산 삭감 우려)

5. 기타 시장 지표

- 미국 10년물 국채 수익률: 4.4087% (+8.2bp)

- 금 가격: $3,403.90 (사상 최고치)

- 달러 인덱스: 3년래 최저치 기록

6. 향후 전망

연준의 독립성에 대한 우려와 미중 무역 갈등의 지속은 시장의 변동성을 높일 것으로 예상됩니다. 투자자들은 향후 발표될 주요 기업들의 실적과 정책 변화에 주목할 필요가 있습니다.

📊 U.S. Stock Market Daily Report

Date: April 21, 2025 (Monday)

Prepared by: GROVERSE Consulting

1. 📉 Major Index Performance

| Index | Closing Value | Change | % Change |

|---|---|---|---|

| Dow Jones Industrial Average | 38,170.41 | -971.82 | -2.48% |

| S&P 500 | 5,158.20 | -124.50 | -2.36% |

| Nasdaq Composite | 15,870.90 | -415.55 | -2.55% |

All three major U.S. indices posted sharp losses of over 2%, with tech-heavy Nasdaq leading the decline.

2. 🔍 Key Market Drivers

▪ Trump’s Pressure on the Fed

Former President Donald Trump harshly criticized Fed Chair Jerome Powell, calling him “Mr. Too Late” and demanding an immediate rate cut. His remarks intensified concerns over the independence of the Federal Reserve, adding to market unease.

▪ U.S.-China Trade Tensions Escalate

China issued a stern warning regarding ongoing trade conflicts and criticized U.S. protectionist policies. Investors fear a renewed breakdown in trade negotiations, raising the specter of global economic instability.

▪ Sharp Decline in Tech Stocks

Major technology firms, dubbed the “Magnificent Seven,” led the sell-off:

- Tesla fell 5.8% amid reports of production delays.

- Nvidia dropped 4.5% following reports that Huawei is ramping up AI chip deliveries.

→ Source: Reuters

3. 📉 Sector Breakdown (S&P 500)

- All 11 sectors closed in the red.

- Biggest losers: Consumer Discretionary and Information Technology

- Least affected: Consumer Staples and Real Estate

4. 🔁 Notable Movers

Top Gainers:

| Company | % Change | Reason |

|---|---|---|

| Discover Financial Services | +3.6% | Merger approval with Capital One |

| Fidelity National Info. Services | +2.4% | Upgraded by Citigroup |

| Netflix | +1.5% | Strong earnings and target price upgrades |

Top Losers:

| Company | % Change | Reason |

|---|---|---|

| Universal Health Services | -10.2% | Medicaid-related revenue concerns |

| Blackstone | -7.8% | Fears of asset sale slowdowns |

| Vistra | -7.7% | Energy budget cut worries |

5. 📈 Other Market Indicators

- 10-Year Treasury Yield: ↑ 4.4087% (up 8.2 bps)

- Gold Price: $3,403.90/oz (new all-time high)

- U.S. Dollar Index: 3-year low

6. 🧭 Outlook & Implications

- Policy uncertainty is intensifying, as Trump’s remarks may influence expectations on Fed action.

- Persistent trade tensions between the U.S. and China are reigniting concerns over global growth.

- Investors are awaiting key earnings reports this week, particularly from mega-cap tech firms, which may sway near-term market direction.

⚠ If market sentiment remains fragile and geopolitical risks persist, further volatility is likely despite any monetary policy adjustments.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

▣ 배경

미국과 중국 간의 무역전쟁은 단기 갈등이 아닌 장기적인 지구력 싸움의 양상을 띠고 있습니다.

- 중국은 국가 주도의 경제구조를 바탕으로 장기 버티기에 자신이 있으며,

- 미국은 연준(Fed)의 금리 인하 정책을 통해 경기 부양 여력을 바탕으로 승기를 잡으려는 전략입니다.

▣ 금리 인하의 목적

연준이 금리를 인하하는 주요 목적은 다음과 같습니다:

- 기업 투자 및 소비 진작

- 금융시장 안정화

- 달러 약세 유도 및 수출 경쟁력 강화

하지만 무역전쟁은 구조적 충격이며, 금리 인하는 경기순환적 도구입니다.

즉, 구조적 문제를 해결하기엔 한계가 있음을 전제로 해야 합니다.

▣ 단기적 시장 반응

| 영향 | 긍정적 효과 | 제한점 |

|---|---|---|

| 주식시장 | 기술주 및 성장주 반등, 유동성 증가 | 무역 불확실성 지속 시 반짝 반등에 그칠 수 있음 |

| 외환시장 | 달러 약세 유도 → 수출기업 호재 | 글로벌 투자심리 위축 시 자금 이탈 우려 |

| 채권시장 | 금리 하락 → 채권가격 상승 | 안전자산 선호 지속 시 효과 제한 |

✅ 2019년 사례: 미국 연준의 금리 인하 이후, 시장은 단기 혼조세를 보였지만 결국 S&P500은 연말 기준 약 29% 상승.

▣ 실물경제에 미치는 영향

| 부문 | 긍정적 효과 | 현실적 한계 |

|---|---|---|

| 소비 | 대출금리 인하 → 가계소비 유도 | 고용 불안, 경기 둔화 시 소비 위축 가능 |

| 기업 투자 | 차입비용 감소 → 투자 유인 | 무역 불확실성이 투자 결정 자체를 미룸 |

| 고용 | 경기 유지 시 고용 방어 가능 | 타격 입는 수출 제조업 중심으로 감원 우려 |

| 부동산 | 주택담보대출 금리 하락 → 주택 수요 증가 | 장기 경기 둔화 시 주택시장 위축 가능 |

▣ 시장 해석의 관건

금리 인하 자체보다 시장이 그것을 어떻게 해석하느냐가 핵심입니다:

| 해석 | 시장 반응 |

|---|---|

| “예방적 조치” → 유동성 확대 | 📈 긍정적 |

| “응급처방” → 경기 침체 우려 반영 | 📉 부정적 |

따라서, 무역전쟁이 장기화되면 금리 인하가 오히려 시장 불안 신호로 작용할 수도 있습니다.

▣ 지구력 게임: 누가 유리한가?

| 국가 | 전략 | 강점 | 약점 |

|---|---|---|---|

| 중국 | 정책적 통제력 기반 장기전 | 중앙집중형 체계, 인내 전략 | 수출 둔화, 해외자본 유출 가능성 |

| 미국 | 금리 인하+소비 기반 내수 유지 전략 | 소비 강세, 금융정책 수단 | 시장심리에 민감, 기업 부채 증가 |

📌 결국 양국 모두 장기 버티기에 들어간다면 금리 인하 효과는 점차 약해지고, 오히려 시장 불안만 증폭될 수 있음.

✅ 결론

- 금리 인하는 단기적으로는 시장 방어에 긍정적 효과가 있지만,

- 무역전쟁이 장기화될수록 한계가 뚜렷해지며,

- 시장은 이를 “경기 침체 대응책”으로 해석할 가능성이 높아집니다.

근본적인 무역 갈등 해소 없이 반복되는 금리 인하는 오히려 시장 불안 신호로 작용할 수 있습니다.

따라서 금리 인하가 시장에 긍정적으로 작용하려면, 동시에 무역협상 진전이라는 정치적 신호도 병행되어야 합니다.

Report in English

🔍 I. Purpose of Interest Rate Cuts in This Context

The Fed typically cuts rates to:

- Stimulate borrowing and investment

- Boost consumer spending

- Ease financial conditions

- Stabilize investor sentiment

But in the context of a trade war, the goal becomes more defensive:

- Offset the shock to business confidence

- Mitigate export weakness

- Cushion declining capital investment

⚖️ II. Trade War as a Structural Shock vs. Rate Cuts as a Cyclical Tool

❗Problem:

Trade wars are structural disruptions (e.g., tariffs, supply chain shifts, geopolitical uncertainty)

🔧 Tool:

Rate cuts are cyclical tools, useful against downturns driven by typical economic slowdowns (e.g., weak demand, low inflation)

⚠ Mismatch Risk: Using interest rate cuts to fight a structural trade war is like “treating a broken bone with painkillers.” You relieve symptoms, not the root cause.

📊 III. Short-Term Market Impact

✅ Positive Effects:

- Boosts stock valuations via lower discount rates (esp. tech and growth stocks)

- Weakens the U.S. dollar, supporting exports

- Improves liquidity and credit conditions

- Fuels risk appetite (equities, corporate bonds rally)

❌ Risks if Trade Tension Persists:

- Markets may interpret rate cuts as signs of desperation, not confidence

- Investors may “fade the rally”, fearing fundamental damage to earnings and global growth

- Confidence-sensitive sectors (e.g., manufacturing, semiconductors) may not rebound

📉 IV. Real Economy Impact

| Factor | Potential Positive Effect | Limiting Factor |

|---|---|---|

| 🏦 Business Investment | Lower financing costs | Trade uncertainty outweighs rate benefits |

| 🛍️ Consumer Spending | Cheaper credit cards, loans | Consumers may delay big purchases if jobs at risk |

| 🏠 Housing | Mortgage rates drop, boosting real estate | If confidence collapses, demand still weak |

| 💼 Employment | Easier borrowing may help hiring | Tariffs may force job cuts in affected sectors |

🔄 V. Endurance Strategy: Who Benefits More from Time?

🇨🇳 China’s Assumption:

- State-led economy can absorb economic pain

- Can stimulate through fiscal tools, central planning

- Less worried about short-term market reactions

🇺🇸 U.S. Assumption:

- Stronger consumer base and monetary tools

- Financial markets are key to confidence → rate cuts aim to cushion them

- Belief: Fed + consumption = resilience

But if rate cuts fail to revive confidence, the U.S. may be at a disadvantage due to:

- High dependence on stock market sentiment

- Corporate debt risks

- Political pressure for economic performance

🧠 VI. Investor Interpretation Matters Most

- If the market sees “preventative cuts” ➝ bullish

- If seen as “emergency stimulus for a broken economy” ➝ bearish

- Repeated cuts with no trade progress ➝ market loses faith in monetary policy

✅ Conclusion

An interest rate cut during a prolonged U.S.-China trade war is a short-term cushion, not a long-term solution. It may temporarily support markets, but its effectiveness weakens if trade tensions persist and structural confidence erodes. For markets to interpret rate cuts positively, either progress in negotiations or a clear economic rebound is needed—otherwise, it signals weakness rather than strength.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

▣ 배경

미국과 중국 간의 무역전쟁은 단기 갈등이 아닌 장기적인 지구력 싸움의 양상을 띠고 있습니다.

- 중국은 국가 주도의 경제구조를 바탕으로 장기 버티기에 자신이 있으며,

- 미국은 연준(Fed)의 금리 인하 정책을 통해 경기 부양 여력을 바탕으로 승기를 잡으려는 전략입니다.

▣ 금리 인하의 목적

연준이 금리를 인하하는 주요 목적은 다음과 같습니다:

- 기업 투자 및 소비 진작

- 금융시장 안정화

- 달러 약세 유도 및 수출 경쟁력 강화

하지만 무역전쟁은 구조적 충격이며, 금리 인하는 경기순환적 도구입니다.

즉, 구조적 문제를 해결하기엔 한계가 있음을 전제로 해야 합니다.

▣ 단기적 시장 반응

| 영향 | 긍정적 효과 | 제한점 |

|---|---|---|

| 주식시장 | 기술주 및 성장주 반등, 유동성 증가 | 무역 불확실성 지속 시 반짝 반등에 그칠 수 있음 |

| 외환시장 | 달러 약세 유도 → 수출기업 호재 | 글로벌 투자심리 위축 시 자금 이탈 우려 |

| 채권시장 | 금리 하락 → 채권가격 상승 | 안전자산 선호 지속 시 효과 제한 |

✅ 2019년 사례: 미국 연준의 금리 인하 이후, 시장은 단기 혼조세를 보였지만 결국 S&P500은 연말 기준 약 29% 상승.

▣ 실물경제에 미치는 영향

| 부문 | 긍정적 효과 | 현실적 한계 |

|---|---|---|

| 소비 | 대출금리 인하 → 가계소비 유도 | 고용 불안, 경기 둔화 시 소비 위축 가능 |

| 기업 투자 | 차입비용 감소 → 투자 유인 | 무역 불확실성이 투자 결정 자체를 미룸 |

| 고용 | 경기 유지 시 고용 방어 가능 | 타격 입는 수출 제조업 중심으로 감원 우려 |

| 부동산 | 주택담보대출 금리 하락 → 주택 수요 증가 | 장기 경기 둔화 시 주택시장 위축 가능 |

▣ 시장 해석의 관건

금리 인하 자체보다 시장이 그것을 어떻게 해석하느냐가 핵심입니다:

| 해석 | 시장 반응 |

|---|---|

| “예방적 조치” → 유동성 확대 | 📈 긍정적 |

| “응급처방” → 경기 침체 우려 반영 | 📉 부정적 |

따라서, 무역전쟁이 장기화되면 금리 인하가 오히려 시장 불안 신호로 작용할 수도 있습니다.

▣ 지구력 게임: 누가 유리한가?

| 국가 | 전략 | 강점 | 약점 |

|---|---|---|---|

| 중국 | 정책적 통제력 기반 장기전 | 중앙집중형 체계, 인내 전략 | 수출 둔화, 해외자본 유출 가능성 |

| 미국 | 금리 인하+소비 기반 내수 유지 전략 | 소비 강세, 금융정책 수단 | 시장심리에 민감, 기업 부채 증가 |

📌 결국 양국 모두 장기 버티기에 들어간다면 금리 인하 효과는 점차 약해지고, 오히려 시장 불안만 증폭될 수 있음.

✅ 결론

- 금리 인하는 단기적으로는 시장 방어에 긍정적 효과가 있지만,

- 무역전쟁이 장기화될수록 한계가 뚜렷해지며,

- 시장은 이를 “경기 침체 대응책”으로 해석할 가능성이 높아집니다.

근본적인 무역 갈등 해소 없이 반복되는 금리 인하는 오히려 시장 불안 신호로 작용할 수 있습니다.

따라서 금리 인하가 시장에 긍정적으로 작용하려면, 동시에 무역협상 진전이라는 정치적 신호도 병행되어야 합니다.

Report in English

🔍 I. Purpose of Interest Rate Cuts in This Context

The Fed typically cuts rates to:

- Stimulate borrowing and investment

- Boost consumer spending

- Ease financial conditions

- Stabilize investor sentiment

But in the context of a trade war, the goal becomes more defensive:

- Offset the shock to business confidence

- Mitigate export weakness

- Cushion declining capital investment

⚖️ II. Trade War as a Structural Shock vs. Rate Cuts as a Cyclical Tool

❗Problem:

Trade wars are structural disruptions (e.g., tariffs, supply chain shifts, geopolitical uncertainty)

🔧 Tool:

Rate cuts are cyclical tools, useful against downturns driven by typical economic slowdowns (e.g., weak demand, low inflation)

⚠ Mismatch Risk: Using interest rate cuts to fight a structural trade war is like “treating a broken bone with painkillers.” You relieve symptoms, not the root cause.

📊 III. Short-Term Market Impact

✅ Positive Effects:

- Boosts stock valuations via lower discount rates (esp. tech and growth stocks)

- Weakens the U.S. dollar, supporting exports

- Improves liquidity and credit conditions

- Fuels risk appetite (equities, corporate bonds rally)

❌ Risks if Trade Tension Persists:

- Markets may interpret rate cuts as signs of desperation, not confidence

- Investors may “fade the rally”, fearing fundamental damage to earnings and global growth

- Confidence-sensitive sectors (e.g., manufacturing, semiconductors) may not rebound

📉 IV. Real Economy Impact

| Factor | Potential Positive Effect | Limiting Factor |

|---|---|---|

| 🏦 Business Investment | Lower financing costs | Trade uncertainty outweighs rate benefits |

| 🛍️ Consumer Spending | Cheaper credit cards, loans | Consumers may delay big purchases if jobs at risk |

| 🏠 Housing | Mortgage rates drop, boosting real estate | If confidence collapses, demand still weak |

| 💼 Employment | Easier borrowing may help hiring | Tariffs may force job cuts in affected sectors |

🔄 V. Endurance Strategy: Who Benefits More from Time?

🇨🇳 China’s Assumption:

- State-led economy can absorb economic pain

- Can stimulate through fiscal tools, central planning

- Less worried about short-term market reactions

🇺🇸 U.S. Assumption:

- Stronger consumer base and monetary tools

- Financial markets are key to confidence → rate cuts aim to cushion them

- Belief: Fed + consumption = resilience

But if rate cuts fail to revive confidence, the U.S. may be at a disadvantage due to:

- High dependence on stock market sentiment

- Corporate debt risks

- Political pressure for economic performance

🧠 VI. Investor Interpretation Matters Most

- If the market sees “preventative cuts” ➝ bullish

- If seen as “emergency stimulus for a broken economy” ➝ bearish

- Repeated cuts with no trade progress ➝ market loses faith in monetary policy

✅ Conclusion

An interest rate cut during a prolonged U.S.-China trade war is a short-term cushion, not a long-term solution. It may temporarily support markets, but its effectiveness weakens if trade tensions persist and structural confidence erodes. For markets to interpret rate cuts positively, either progress in negotiations or a clear economic rebound is needed—otherwise, it signals weakness rather than strength.

<본 정보는 투자 자문이 아니며, 투자 결정은 신중한 판단 하에 이루어져야 합니다. 투자에 따른 책임은 투자자 본인에게 있으며, 그로버스 컨설팅은 투자 결과에 대한 책임을 지지 않습니다.>

📩 문의: john.groverse@gmail.com / KaKao : groverse / Tel : 0954 156 0473

1. 전략의 핵심 프레임: “버티는 자가 이긴다”

- 미국은 체면과 정치적 프레임을 지키기 위해 실질적 양보보다 중국의 항복 제스처를 더 중요하게 간주

- 중국은 체제 특성상 언론 통제와 민족주의 결속을 통해 장기전 버티기 전략 선택

- 양국은 모두 실익보다 ‘굴복하지 않았다’는 명분을 중시함

2. 시기별 전개 시나리오

✅ 4~5월: 기싸움 극대화 단계

- 미국: 유럽, 일본, 멕시코 등과의 무역 진척 발표 → “중국을 제외한 글로벌 협력 연출”

- 중국: 반격 수위 유지, 내부 결속 강조 → 공식적 유화 제스처 없음

- 목적: 중국 고립 구도 형성 + 시장 안정화 무대 준비

✅ 6월: 금리 인하 기대 시점 → 미국의 전략적 전환점

- 연준의 금리 인하 기대 → 시장 반등 + 인플레이션 안정 → 트럼프의 경제적 자신감 상승

- 중국과의 공식 협상은 여전히 없음. 미국은 버티기 유지

✅ 7~8월: 중국의 유화 제스처 + 미국의 봉합 진입

- 중국: 일부 수입 확대, 무역 조건 완화 등 형식적 양보 발표 가능성

- 미국: “중국이 무릎 꿇었다” 프레임으로 협상 공식화 및 봉합 전환

- 증시: 글로벌 리스크 완화 기대감으로 급반등 흐름 가능성

3. 구조적 동기: 미국 재정적자와 협상 연계 전략

- 미국은 동맹국 및 무역 파트너에게 재정 기여 및 무역 균형 개선 요구 강화

- 관세정책은 더 이상 보호무역이 아닌 재정 회복과 체면 유지를 위한 협상 지렛대

- 핵심 메시지: “우리가 리더십을 행사하려면, 상대도 대가를 치러야 한다”